Practice Update March 2020

Phillip Borg • 1 March 2020

MYEFO 2019-20

The 2019-20 mid-year economic fiscal outlook (MYEFO) released on 12 December 2019 shows the government is maintaining a budget surplus for 2019-20 but it has been reduced from $7.1 billion to $5 billion.

Tax changes in MYEFO

There is only one minor new tax change announced in MYEFO, which provides a discretion to the Commissioner of Taxation to direct taxpayers to undertake an approved training course on record keeping instead of being subject to financial penalties.

While the Commissioner already has a discretion to remit penalties, where he sees fit, this announcement allows him to make such a remission subject to the taxpayer undertaking record keeping training.

Draft legislation released on STP reporting of child support payments

In January, Treasury released exposure draft legislation which proposes to expand the single touch payroll (STP) regime to include the voluntary reporting of child support information. First announced in the 2019 Budget, the aim of the proposed legislation is to reduce the compliance burden on employers and individuals reporting to multiple government agencies. Explanatory materials are also available on the Treasury website.

Small business support for bushfire affected communities

On 20.01.2020, the Federal Government announced a range of measures to support small business affected by bushfires including:

Top-up grants of up to $50,000 in grant funding (tax free) for eligible small businesses and non-profit organizations under the Disaster Recovery Funding Arrangements.

Loans of up to $500,000 for businesses that have suffered significant asset loss or a significant loss of revenue.

$3.5 million to establish the Small Business Bushfire Financial Support Line as well as to fund 10 additional financial counsellors with the ability to provide advice to around 100 small businesses a day.

28 May 2020 extension to lodge and pay business activity statements and income tax returns.

Flexibility in quarterly Pay-As-You-Go Instalments to vary these instalments to zero for the December 2019 quarter and claim a refund for any instalments made in September 2019 quarter.

We will keep you informed on any further developments.

Taxable payments reporting for businesses hiring cleaning or courier contractors

Over the summer holiday season some businesses used more cleaning and courier contractors, and therefore may need to lodge a Taxable Payments Annual Report (TPAR) in August 2020.

Typically, the types of businesses making increased contractor payments to cleaning and courier services, are:

Event management and building maintenance, property management businesses engaging contractors to provide cleaning services.

Florists and other retail businesses engaging contractors to provide courier services.

In these circumstances, your business will need to report if they:

Have an Australian business number (ABN).

Pay contractors to provide courier or cleaning services on their behalf.

Provide cleaning or courier services, and the payments they receive for these services make up 10% or more of their total GST turnover, even if their business is not registered for GST.

If you are not sure whether your business needs to complete a TPAR, check the ATO’s website or talk to us.

Taxpayer fails to prove income tax assessment was excessive nor entitled to ITCs

Jarvis Lavery v FC of T 2019 AATA 5409

The AAT has found that a taxpayer could not establish that his income tax assessment was excessive nor that he was entitled to input tax credits (ITCs) for certain acquisitions.

The taxpayer was involved in music, television and film production and conducted a share trading business.

Following a tax audit, the ATO determined that the taxpayer had understated income and over-claimed ITCs. The Commissioner increased the taxpayers tax liabilities with penalties. The taxpayer’s objection to assessments, was wholly disallowed by the Commissioner. The taxpayer then sought a review of the objection decisions in the AAT.

There was a substantial number and value of deposit entries in bank accounts held or controlled by the taxpayer which the Commissioner considered to be “unexplained”. The GST dispute concerned whether the taxpayer had made and paid for acquisitions from an associated entity for which ITCs were claimed, and whether other acquisitions were business and not of private or domestic nature.

The taxpayer was unable to produce accurate records to substantiate the claims.

While the Commissioner conceded that the taxpayer was entitled to ICs on acquisitions relating to his share trading business, these were reduced credit acquisitions, while maintaining the income tax assessment was not excessive.

The AAT found that the taxpayer was unable to establish that the income tax assessment was excessive nor that there was any entitlement for ITCs for the relevant acquisitions.

Despite the voluminous “reconciliation” and supporting bank and credit card statements, the AAT said that it was “simply impossible” to calculate the taxpayer’s assessable income. Accordingly, it was not satisfied that the income tax assessment was excessive.

The AAT agreed with the Commissioner that the taxpayer was entitled to ITCs on acquisitions relating to his share trading business at a reduced rate, while not being persuaded that the taxpayer provided evidence for having made creditable acquisitions from the associated entity. The AAT held the remaining acquisitions were made in the course or furtherance of an enterprise but were of a domestic or private nature.

Welfare recipients to benefit from reporting simplification

On 28.01.2020, the Morrison Government announced an overhaul of the way welfare recipients report employment income resulting in savings of $2.1 billion over the Federal Budget Forward Estimates.

Under the changes more than 1.2 million welfare recipients who earn an income each year will be able to report their fortnightly earnings to Centrelink as it appears on their payslip.

Currently recipients must undertake a calculation to report their or their partner’s earnings based on the number of shifts they have worked and the hourly rate rather than the amount they were actually paid.

Minister for Families and Social Services Anne Ruston said the reform was delivering on the Government’s commitment to simplify the payments system.

“We want to make sure that Australians who need financial support are able to get the support that they are eligible for – no less and no more,” Minister Ruston said.

“The current system of calculating earnings can be confusing and lead to misreporting especially when accounting for overtime or penalty rates.

“These changes will make accurate reporting much easier for people getting a social security payment.”

This change will also facilitate the use of Single Touch Payroll data over the 12 months to July 2021, which will mean welfare recipients can have their employment and income details pre-filled similar to online tax returns.

Draft legislation will be released for consultation and the Government will introduce the Bill when Parliament resumes.

People who receive Newstart, Youth Allowance and other social security payments will still need to report their income every fortnight either online, via the mobile app, over the phone or by visiting a Centrelink service centre.

Illegal early release of super

Withdrawing your super early unless you meet a condition of release is illegal.

Generally, you can only withdraw your super when you reach retirement.

There are limited circumstances where you can legally withdraw your super early, such as:

specific medical conditions

if you are experiencing severe financial hardship.

Super laws provide specific rules for when you can withdraw your super. These are called conditions of release.

Beware of people promoting early release of super schemes. They might tell you they can help you withdraw your super to pay off credit card debt, buy a house or car, or go on a holiday. These schemes are illegal.

Illegal schemes will cost you a lot more than the super you withdraw and will get you into trouble. There are severe fees and penalties. Promoters of schemes encouraging the illegal early release of super may face prosecution and civil or criminal penalties.

Changes to Research & Development (R & D)

The Treasury Laws Amendment (Research and Development Tax Incentive) Bill 2019 was passed by the House of Representatives in February.

The Bill proposes to:

Cap the refundability of the R&D tax offset at $4 million per annum.

Increase the R&D expenditure threshold from $100 million to $150 million and making the threshold a permanent feature of the law.

Link the R&D tax offset rate for the refundable R&D offset to claimants’ corporate tax rates plus a 13.5 percentage point premium.

Change the existing flat premium available to non-refundable offset claimants to one that increases a company’s research and development (R&D) intensity increases.

Directly extend the general anti-avoidance rules in the tax law to R&D offsets; and

Provide for the publication of information about Incentive claimants and their R&D expenditure.

We will keep you informed on further developments concerning the passage of this legislation.

FBT exemption will now include ride sharing services

Legislative amendments have been introduced into Federal Parliament to the existing fringe benefits tax (FBT) exemption for certain taxi travel to include a broader range of transport services including ride sharing services.

The Treasury Laws Amendment (2019 Measures No. 3) Bill 2019 will deal with the current situation where the FBT exemption now only applies to taxis. This exemption is used by employers to allow employees to sometimes travel to and from work with a particular focus on employees living in the inner city.

The change will apply to the 2019-20 FBT year onward.

Important checks for employers when hiring a contractor

There’s not just one deciding factor that makes a worker you hire an employee or contractor for tax and superannuation purposes.

As an employer, it’s a decision you can only make once you’ve reviewed the entire working arrangement.

It’s important to assess this correctly because getting it wrong will put your business at risk of penalties and charges. Failing to pay your workers their correct entitlements is a costly mistake.

To get to the right answer, you need to consider a number of factors. Before hiring a contractor review the following case scenarios:

Ability to subcontract or delegate – if they pay someone else to do the work.

Basis of payment – if they will be paid based on an agreed quote they provided.

Equipment, tools and other assets – if they are providing their own tools and equipment needed to get the job done.

Commercial risks – if they are legally responsible for their work and liable for fixing mistakes or defects.

Control over the work – if they decide how the work gets done subject to specific terms in any contract or agreement.

Independence – if they operate their own business independently of your business.

If the answer is NO to some or all of these scenarios, you need to seek further information and advice before treating your worker as a contractor.

Case Study – Super Guarantee payable for building site worker who was held NOT to be an independent contractor

This Administrative Appeals Tribunal case confirmed the ATO’s decision that a person who provided services as part of an asbestos removal/building renovations business was an employee and not an independent contractor.

This issue is a ticking time bomb for thousands of SMEs who after taking advice mistakenly believe a carefully drafted contract will absolve them any obligation to pay statutory superannuation.

However, as usual the focus of the AAT was not what a contract says but what actually happens in practice.

Below is an extract of the relevant contract.

I, [Mr Wheeler]

Herby agree that I contract to KBE Contracting Australia and will pay my own tax.

I’m not entitled to Holiday pay or Sick Leave.

The hourly rate that I am being paid includes an allowance that I will make my own superannuation contribution and no claim will be made against KBE Australia, Directors or Associated Companies.

The evidence suggested that Mr Wheeler was a common law employee because he:

Did not perform the work as an entrepreneur operating his own business; and

He performed work in and for the business of the employer.

There was no evidence of that the worker had transactional systems such as payment and debt collection systems, financial records, budgets and forecasting systems, as well as an absence of risk on the part of the worker.

This case is significant because it results in a non-tax-deductible superannuation guarantee charge payment of $15,000. Note this is in respect to one person, to state the obvious, if there were 10 working under this arrangement, then the SGC charge would have been 150k. A potentially crippling charge to a small business. Due to increasing awareness in the marketplace, employers engaging individual contractors (who work under their contract and direction) need to carefully review existing arrangements.

Donations

So, you’re sitting opposite your accountant and the subject of donations comes up… “Have you made any tax-deductible donations in the last tax year” etc.

Quite often donations are made at shopping centres, supermarkets, check-outs and social functions but records not kept.

However, if you don’t have the documentary proof (or access to) then you can’t make a claim.

Quite often people donate to “Go Fund Me” pages on social media and some of these are for worthy causes.

When can you claim a tax deduction for a gift or donation?

You can claim a tax deduction for a donation of cash of $2 or more made to an organisation that is endorsed by the ATO as a Deductible Gift Recipient (DGR). DGRs include Public Benevolent Institutions like the Australian Red Cross Society, or organisations established to prevent or relieve the suffering of animals like Wildlife Victoria Inc.

The Australian Business Number Register allows potential donors to check whether an organisation has DGR status and the date at which they obtained this status. Importantly, if the organisation does not have DRG status when a donation is made, a tax deduction cannot be claimed (unless the organisation subsequently obtains DGR status and has the endorsement backdated to an earlier date).

Note that if you receive any benefit or consideration for the expenditure, then you cannot claim a tax deduction. An example of this could be raffle tickets or outlay for a social function such as a charity ball.

While it is not unknown for some DRGs to issue tax deductible receipts for such expenditure, we suggest this is reckless on their part as it only endangers their DGR status.

We mention in passing the Treasury Laws Amendment (2019-20 Bushfire Tax Assistance) Bill 2020 is an extension of DGR status to two new charitable trusts, the Australian Volunteers Trust and the Community Building Trust.

A common complaint of donors is that they don’t know how donations will be applied and indeed, to what degree those donations are depleted by the DGR’s administrative expenses. It is important to note that DRGs are subject to strict supervision and are overseen by the ATO and (usually) the Australian Charities and Not-for-profits Commission (ACNC). They are restricted to applying their assets and income toward the approved purpose or purposes for which the organisation was established and is maintained, and all expenses must be consistent with that.

While many charities publicity share the stories of their charitable works, a more detailed view of how a charity manages the donations it receives can be obtained by looking them up on the ACNC Charity Register. Registered charities are required to lodge an annual information statement, and depending on their size, may also be required to lodge audited financial statements. These documents are made publicly on the ACNC Charity Register.

To maximise tax effectiveness for donations it is suggested that you choose 3-4 DGRs, make larger but affordable donations and essentially retain receipts.

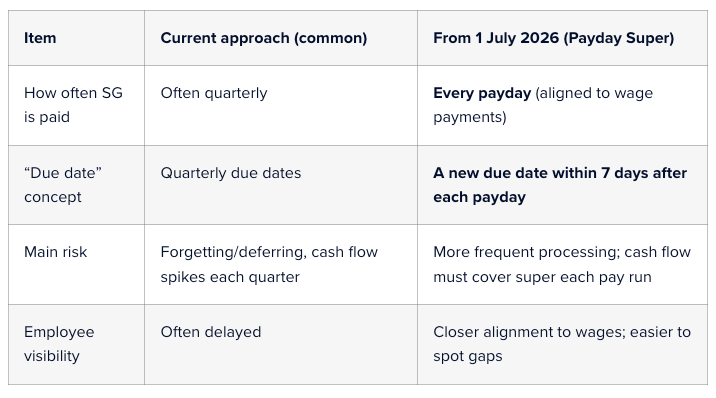

Cashflow red flags for small business in 2026

Readiness strategies in preparation for the Payday Super If you run a small business, paying Superannuation can feel like “one more admin job” on top of payroll, BAS and everything else. Two key changes mean Superannuation deserves a fresh look this year: The Super Guarantee (SG) rate is 12% for 1 July 2025 to 30 June 2026 (and remains 12% after that). From 1 July 2026, “Payday Super” starts — employers will be required to pay SG on payday , rather than quarterly, and contributions must be paid into the employee’s fund within 7 days of payday . What does SG at 12% mean in everyday terms? SG is calculated on an employee’s Ordinary Time Earnings (OTE) (often the base rate and ordinary hours, plus certain loadings/allowances depending on how they’re paid). The key point for most businesses is that the Superannuation cost is now 12 cents for every $1 of OTE. If you haven’t already, it’s worth confirming whether your staff packages are “plus super” (super on top) or “inclusive of super” (rare, but it happens). A small misunderstanding here can quietly create underpayments. What is “Payday Super” and why is it changing? Many employers pay the Superannuation Guarantee (SG) quarterly. Payday Super changes the rhythm: From 1 July 2026 , each time you pay OTE to an employee, it creates a new super payment obligation for that payday. You’ll have a 7-day due date for the SG to arrive in the employee’s fund after each payday (this is designed to allow time for payment processing). The ATO is implementing the change, and guidance is already being published to help employers prepare. This reform is aimed at reducing unpaid super and making it easier for workers to see whether super has actually been paid, closer to when they’re paid wages. Quarterly vs payday Super

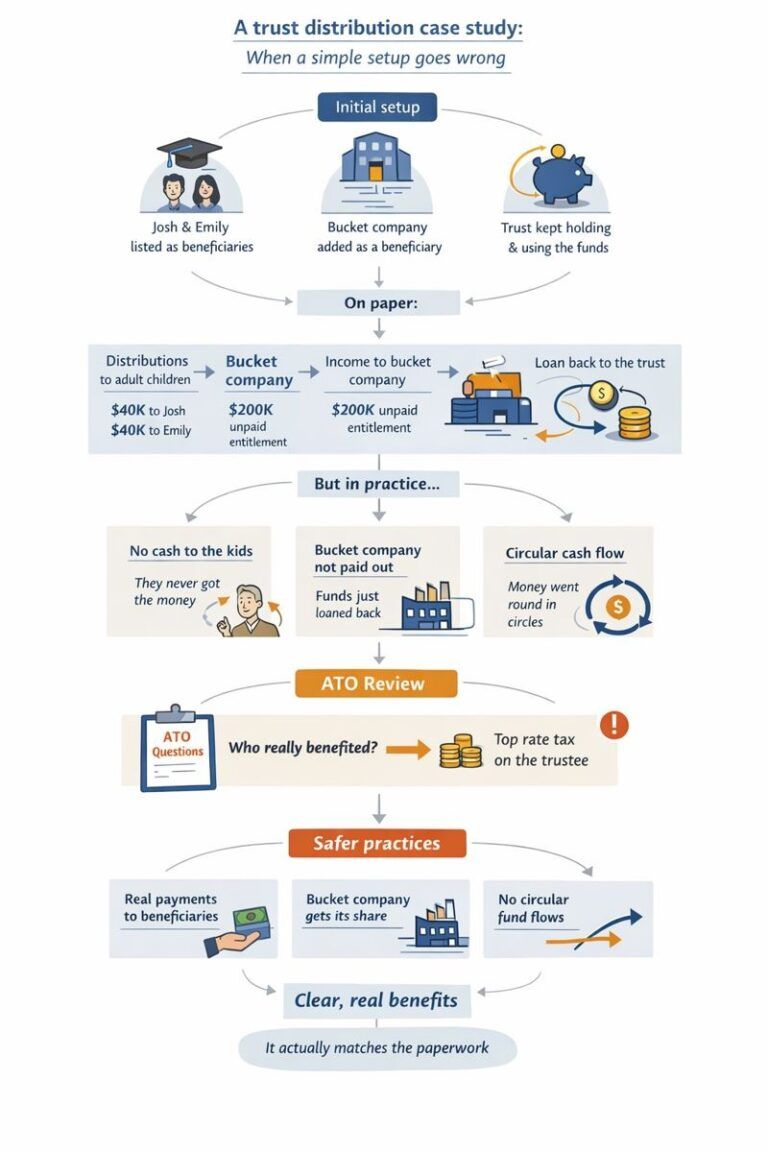

A real-world case study on trust distributions Mark and Lisa had what most people would describe as a “pretty standard” setup. They ran a successful family business through a discretionary trust. The trust had been in place for years, established when the business was small and cash was tight. Over time, the business grew, profits improved, and the trust started distributing decent amounts of income each year. The tax returns were lodged. Nobody had ever had a problem with the ATO. So naturally, they assumed everything was fine. This is where the story starts to get interesting. Year one: the harmless decision In a good year, the business made about $280,000. It was suggested that some income be distributed to Mark and Lisa’s two adult children, Josh and Emily. Both were over 18, both were studying, and neither earned much income. On paper, it made sense. Josh received $40,000. Emily received $40,000. The rest was split between Mark, Lisa, and a company beneficiary. The tax bill went down. Everyone was happy. But here’s the first quiet detail that mattered later. Josh and Emily never actually received the money. No bank transfer. No separate accounts. No conversations about what they wanted to do with it. The trust kept the funds in its main business account and used them to pay suppliers and reduce debt. At the time, nobody thought twice. “It’s still family money.” “They can access it if they need it.” “We’ll square it up later.” These are very common thoughts. And this is exactly where risk quietly begins. Year two: things get a little more complicated The next year was even better. They used a bucket company to cap tax at the company rate. Again, a common and legitimate strategy when used properly. So the trust distributed $200,000 to the company. No cash moved. It was recorded as an unpaid present entitlement. The idea was that the company would get paid later, when cash flow allowed. Meanwhile, the trust needed funds to buy new equipment and cover a short-term cash squeeze. The trust borrowed money from the company. There was a loan agreement. Interest was charged. Everything looked tidy on paper. From the outside, it all seemed sensible. But economically, nothing really changed. The trust made money. The trust kept using the money. The same people controlled everything. The bucket company never actually used the funds for its own business or investments. This detail becomes important later. Year three: circular money without anyone realising By year three, things had become routine. Distributions were made to the kids again. The bucket company received another entitlement. Loans were adjusted at year-end through journal entries. What is really happening is a circular flow. Money was being allocated to beneficiaries, then effectively coming back to the trust, either because it was never paid out or because it was loaned back almost immediately. No one was trying to hide anything. No one thought they were doing the wrong thing. They were just following what they’d always done. This is how section 100A issues usually arise. Slowly, quietly, and without any single dramatic mistake.