Blog

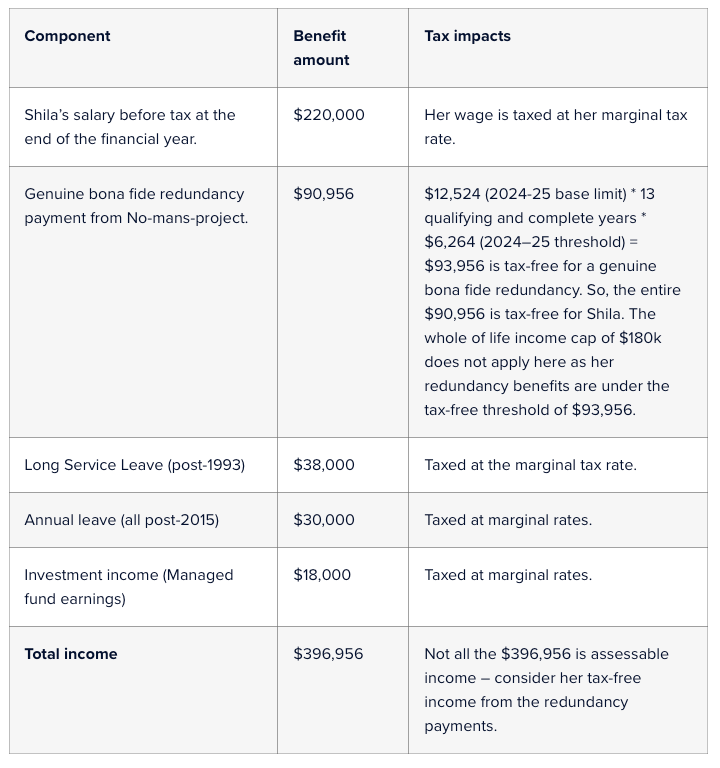

Shila is taking the leap

Key concerns when selling a business in: A strategic guide for business owners

Strategies for individuals before June 30, 2025

Strategies for individuals before June 30, 2025

A foreign entrepreneur’s guide to starting a business in Australia Starting a business as a foreign entrepreneur can be an exhilarating way to access new markets, diversify investment portfolios, and create fresh opportunities. Many countries around the globe provide pathways for non-residents and foreign nationals to register businesses. However, understanding different countries’ legal requirements, procedures, and opportunities is crucial for success. In this issue, we will navigate the process of establishing a business in Australia to help foreign entrepreneurs looking to register a company in Australia. Key takeaways Foreign entrepreneurs can fully own Australian businesses with no restrictions on ownership. Registered office and resident director requirements are key legal considerations. ABN and ACN are essential for business registration. The application process can be done online, simplifying the process for foreign entrepreneurs. Why register a business as a foreign entrepreneur? There are various reasons why a foreigner may want to register a company in another country. These reasons include expanding into a foreign market, taking advantage of favourable tax laws, leveraging local resources, or benefiting from business-friendly regulatory environments. Before registering, conducting thorough market research to assess whether establishing a business abroad aligns with your objectives is essential. Understanding the country’s political and economic climate, legal framework, and tax system will help ensure the success of your venture. The general process for registering a business as a foreign entrepreneur While the exact requirements may differ from country to country, some common steps apply to most jurisdictions when registering a company as a foreign entrepreneur: Choosing the business structure The first step is deciding on the appropriate business structure. The structure determines liability, taxation, and governance. Common types of business structure include: Sole proprietorship: A single-owner business where the entrepreneur has complete control and entire liability. Limited Liability Company (LLC): Offers liability protection to the owners, meaning their assets are not at risk. Corporation (Inc.): A more complex structure that can issue shares and offers limited liability to its shareholders. Different countries have varying rules regarding foreign ownership, so understanding the options available is essential before registering a company. Registering with local authorities Regardless of the jurisdiction, most countries require you to register your company with the relevant local authorities. This process typically includes submitting documents such as: Company name and business activities: You need to choose a unique company name that adheres to local naming regulations. Articles of incorporation: This document outlines the company’s structure, activities, and bylaws. Proof of identity : As a foreign entrepreneur, you will likely need to provide a passport and other identification documents. Proof of address: Many countries require a physical address for the business, which may be the address of a registered agent or office. Tax Identification Number (TIN) and bank accounts After registering the company, you will typically need to apply for a tax identification number (TIN), employer identification number (EIN), or equivalent, depending on the jurisdiction. This number is used for tax filing and reporting purposes. Opening a business bank account is another critical step. Some countries require a local bank account for business transactions, and you may need to visit the bank in person or appoint a local representative to help with the process. Complying with local regulations Depending on the type of business, specific licenses and permits may be required to operate legally. For example, food service, healthcare, or transportation companies may need specific licenses. Compliance with local labour laws and intellectual property protections may also be necessary. Appoint directors and shareholders To register a company, you’ll need to appoint at least one director who resides in Australia. The director will be responsible for ensuring the company meets its legal obligations. You will also need to appoint shareholders, who can be either individuals or corporations. For foreign entrepreneurs, the requirement for a resident director is one of the key challenges. If you don’t have a trusted individual in Australia to act as the director, you can engage a professional service to fulfil this role. This ensures your business remains compliant with local regulations. Choose a company name Next, you need to choose a company name. The name should reflect your business but must be unique and available for registration. You can check the availability of a name through the Australian Securities & Investments Commission (ASIC) website. Remember that the name must meet legal requirements and cannot be similar to an existing registered company. If you’re unsure, seeking professional advice is always a good move. Apply for an Australian Business Number (ABN) and Australian Company Number (ACN) Once you’ve selected your business structure and appointed your directors, it’s time to apply for an Australian Business Number (ABN) and an Australian Company Number (ACN). These are essential for running your business in Australia. ABN: This unique 11-digit number allows your business to interact with the Australian Taxation Office (ATO) and other government agencies. ACN: This 9-digit number is allocated to your company upon registration with ASIC and serves as your business’s unique identifier. You can easily apply for both numbers online through the Australian Business Register (ABR) and the ASIC websites. Register for Goods and Services Tax (GST) If your business expects to earn more than $75,000 in revenue annually, you must register for GST. This means your business will charge customers an additional 10% on goods and services. The GST registration threshold for non-profit organisations is higher at $150,000 annually. If your company is below these thresholds, registering for GST is optional, but registration becomes mandatory once it exceeds the limit. Set up a registered office Every Australian company must have a registered office in Australia. This is where all official government documents, including legal notices, are sent. You can use your premises or hire a foreign company registration service to provide a virtual office address. Common challenges for foreign entrepreneurs While the process is relatively simple, there are a few hurdles that foreign entrepreneurs may encounter when registering a company in Australia: Resident director requirement: You’ll need a director residing in Australia. If you don’t have one, you’ll need to engage a service provider to fulfil this role. Understanding local tax laws: Australia has a corporate tax rate of 25% for small businesses with annual turnovers of less than $50 million. However, larger companies with turnovers exceeding $50 million are subject to a standard corporate tax rate of 30%. Foreign entrepreneurs must also understand the implications of the Goods and Services Tax (GST) and payroll tax. Compliance with Australian regulations: Navigating Australia’s various regulations and compliance requirements can be time-consuming. An accountant or adviser can help you in this regard. FAQs Can I register a company in Australia as a foreigner? Yes, foreign entrepreneurs can register a company in Australia. The only requirement is to have a resident director. Do I need to be in Australia to register a company? No, you can complete the registration process online. However, you must appoint a resident director. Do I need an Australian bank account to start a business in Australia? You will need an Australian bank account to handle your business’s finances and transactions. Can I operate my Australian company from abroad? Yes, you can operate your company remotely, but you must comply with all local tax laws and regulations.

Do bucket companies help build wealth at retirement? Bucket companies are familiar with wealth-building strategies, particularly as individuals approach retirement. By distributing profits to a bucket company, individuals can benefit from reduced tax liabilities and enhanced investment growth opportunities. This essay explores how bucket companies influence wealth building at retirement, their impact on age pension eligibility and tax positions, and strategies to maximise economic outcomes. Understanding bucket companies A bucket company is used to receive distributions from a family trust. Instead of distributing profits directly to individuals, which may attract high marginal tax rates, the trust distributes income to the bucket company, which is taxed at the corporate tax rate (currently 30% or 25% for base rate entities). The company can then retain the after-tax profits for reinvestment or distribution. Impact on wealth building at retirement Tax efficiency and compounding growth Using a bucket company can result in significant tax savings compared to personal marginal tax rates, reaching up to 47% (including the Medicare levy). Retained earnings within the bucket company are taxed lower, allowing more capital to compound over time. Example of Tax Efficiency: Income DistributedPersonal Marginal Tax (47%)Bucket Company Tax (25%)Savings $100,000$47,000$25,000$22,000 Over 20 years, if the tax savings of $22,000 per year are reinvested at an annual return of 7%, they would accumulate to approximately $1,012,000. Age pension and means testing The age pension is subject to both an income test and an assets test. Holding wealth in a bucket company can impact these tests: Income Test: Distributions to individuals count as assessable income. Retained profits within the company do not. Assets Test: The value of the bucket company shares is counted as an asset, which may affect pension eligibility. Strategic use of the company can help individuals control their assessable income, potentially increasing their age pension entitlement. Strategies to maximise economic outcomes Timing of Distributions By deferring distributions from the bucket company until retirement, individuals can benefit from lower marginal tax rates or effectively use franking credits. Dividend Streaming Using franking credits from company-paid tax can reduce personal tax liabilities when distributed dividends. Investment within the Company Reinvesting retained earnings within the bucket company in diversified assets can enhance compounding returns. Family Trust Distribution Planning Strategically distributing income to lower-income family members before reaching the bucket company can reduce overall tax. Winding Up or Selling the Company Carefully planning an exit strategy to wind up the b ucket company or sell its assets can minimise capital gains tax liabilities. Example of a retirement strategy with a bucket company Assume that John and Mary, aged 65, have distributed $100,000 annually from their family trust to their bucket company over 20 years. Corporate tax paid: 25% Annual return on reinvestment: 7% After-tax reinvested earnings annually: $75,000 YearAnnual ReinvestmentTotal Accumulated Amount (7% p.a.)5$75,000$435,30010$75,000$1,068,91420$75,000$3,867,854 At retirement, they can distribute dividends with franking credits to minimise personal tax and supplement their income while potentially qualifying for some age pension benefits due to strategic income timing. FAQ What is a bucket company? A bucket company is a corporate entity that receives trust distributions, taxed at the corporate rate rather than personal marginal rates. How does a bucket company impact my age pension eligibility? While retained earnings do not affect the income test, the value of the company shares is considered an asset under the assets test. Can bucket companies help reduce tax during retirement? Yes, by using franking credits and strategic distribution timing, bucket companies can minimise tax liabilities. Are there risks associated with using bucket companies for retirement planning? Yes, risks include changes in tax laws, corporate compliance costs, and potential capital gains tax upon winding up the company. Should I consult a professional before using a bucket company? Absolutely. Professional advice is essential to ensure compliance with tax laws and optimise wealth-building strategies.

Personal super contribution and deductions

Don’t let taxes dampen your holiday spirit! Just like Santa carefully checks who’s naughty or nice, businesses need to watch the tax rules when spreading Christmas cheer. Hosting festive parties for employees or clients can lead to Fringe Benefits Tax (FBT). FBT is a tax employers pay when they provide extra perks to employees, their families, or associates. It’s separate from regular income tax and is based on the value of the benefit. The FBT year runs from 1 April to 31 March, and businesses must calculate and report any FBT they owe. With a bit of planning—just like Santa’s perfect delivery route—you can celebrate while keeping your tax worries in check! FBT exemption: A little Christmas gift from the taxman The tax rules include a “minor benefit exemption”—like a small stocking stuffer. If the benefit given to each employee costs less than $300 and isn’t a regular thing, it’s exempt from Fringe Benefits Tax (FBT). Christmas parties fit perfectly here because they’re one-off events. Businesses can avoid FBT hassles if the cost per employee stays under $300. Remember: the more often you give out perks, the less likely they’ll qualify for this exemption. Thankfully, Christmas only comes once a year! Christmas parties at the office If you host your Christmas party at your business premises during a regular workday, costs like food and drinks are FBT-free, no matter how much you spend. However, you can’t claim a tax deduction or GST credits for those expenses. If employees’ family members join and the cost per person is under $300, there’s still no FBT, but again, no tax deduction or GST credits can be claimed. However, FBT will apply if the cost is over $300 per person. The good news is that you can claim both a tax deduction and GST credits in that case. FBT check for Christmas parties at the office Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Employees onlyUnlimitedNoNoEmployees and their familyLess than $300NoNoMore than $300YesYesClientsUnlimitedNoNo Think of it like this: at your Christmas party, the food and drinks are like Santa’s bag of gifts – no dollar limit exists for employees enjoying them on business premises. But if you add a band or other entertainment, the costs can add up quickly, and if the total cost per employee exceeds $300, FBT kicks in. Keep it under $300 per person, and you’re in the clear. Christmas parties outside the office If you hold your Christmas party at an external venue, like a restaurant or hotel, it’s FBT-free as long as the cost per employee (including their family, if they come) is under $300. But remember, you can’t claim a tax deduction or GST credits in this case. FBT will apply if the cost exceeds $300 per person, but you can claim a tax deduction and GST credits. Good news: employers don’t have to pay FBT for taxi rides to or from the workplace because there’s a special exemption. FBT check for Christmas parties outside the office Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Employees onlyLess than $300NoNoMore than $300YesYesEmployees and their familyLess than $300NoNoMore than $300YesYesClientsUnlimitedNoNo Clients at the Christmas party If clients attend the Christmas party, there’s no FBT on the expenses related to them, no matter where the party is held. However, you can’t claim a tax deduction or GST credits for part of the costs that apply to clients. Christmas gifts Many employers enjoy giving gifts to their employees during the festive season. If the gift costs less than $300 per person, there’s no FBT, as it’s usually not considered a fringe benefit. FBT check for Christmas gifts Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Entertainment giftsLess than $300NoNoMore than $300YesYesNon-entertainment giftsLess than $300NoYesMore than $300YesYes However, FBT might apply if the gift is for entertainment. Entertainment gifts include things like tickets to concerts, movies, or holidays. Non-entertainment gifts—like gift hampers, vouchers, flowers, or a bottle of wine—are usually FBT-free if under $300. So spread the festive cheer, but keep an eye on the taxman to avoid surprises!

6-year rule