Practice Update October 2021

LEGISLATION UPDATES

PAID PARENTAL LEAVE SCHEME BILL INTRODUCED

Legislation introduced into Parliament on 25.8.2021 will allow parents to count the period they have received the COVID-19 Disaster Payment towards the work test for Parental Leave Pay (PLP) and Dad and Partner Pay(DaPP).

This will come as welcome relief for families living in extended lockdown conditions. The change will help parents who have had their hours of work reduced or stood down during the recent outbreaks retain their eligibility for the payments under the Paid Parental Leave Scheme.

The change will also support families who have received the COVID-19 Disaster Payment to meet the work test and will apply to anyone who receives the payment in the future.

The amendments, included in the Paid Parental Leave Amendment (COVID-19 Work Test) Bill 2021, follow a similar approach in 2020 where time spent receiving the JobKeeper payment counted towards the Paid Parental Leave work test.

Primary carers of a newborn can receive Parental Leave Pay for up to 18 weeks which can be transferred to the other parent at any time should they take over primary caring responsibilities. Flexibility measures introduced last year also allow the final six weeks to be shared or taken by either parent at any time until their child turns 2. In addition, Dad and Partner Pay is available for two weeks. Both payments are paid at the national minimum wage of $772.55 per week.

Families may also be eligible for Family Tax Benefit Part A up to $191.24 per child a fortnight for children up to 12 and Part B up to $162.54 per family a fortnight for children under 5.

BILL INTRODUCES REPORTING REGIME FOR THE SHARING ECONOMY

Legislation to implement a reporting regime for the sharing economy was introduced into Parliament on 25 .8. 2021.. The Bill requires operators of online marketplaces or electronic distribution platforms (EDPs)to report seller identification and payment details relating to transactions facilitated through their platform to the Australian Taxation Office (ATO).

The sharing economy has grown significantly over recent years. There is a risk that some sellers who use these platforms are not reporting their full income or paying the right amount of tax. The reporting regime helps ensure that sharing economy sellers meet their tax obligations and do not have an unfair advantage compared to similar activity elsewhere in the economy due to poor tax compliance. Key players in the sharing economy include Airbnb, Uber, and Lyft.

The Treasury Laws Amendment (2021 Measures No.7) Bill 2021 will:

- require electronic platform operators to provide information on transactions made through the platform to the ATO

- facilitate the closure and any transitional arrangements associated with Australian Financial Complaints Authority replacing the Superannuation Complaints Tribunal; and

- removes the $250 non-deductible threshold for work-related self-education expenses.

SUPPORTING MORE SMALL AND MEDIUM-SIZED BUSINESSES TO ACCESS FUNDING

The Federal Government is providing additional support for (SMEs) who continue to deal with the economic impacts of the COVID‑19 crisis by expanding eligibility for the SME Recovery Loan Scheme.

In recognition of the continued economic impacts of COVID‑19, the Government will remove requirements for SMEs to have received JobKeeper during the March quarter of 2021 or to have been a flood-affected business to be eligible under the SME Recovery Loan Scheme.

As with the existing scheme, SMEs dealing with the coronavirus’s economic impacts with a turnover of less than $250 million will be able to access loans of up to $5 million over a term of up to 10 years. Other key features of the SME Recovery Loan Scheme include:

- The Government guarantee will be 80 per cent of the loan amount.

- Lenders are allowed to offer borrowers a repayment holiday of up to 24 months.

- Loans can be used for a broad range of business purposes, including to support investment.

- Loans may be used to refinance any pre-existing debt of an eligible borrower, including those from the SME Guarantee Scheme.

- Loans can be either unsecured or secured (excluding residential property).

The expanded scheme will enable lenders to continue supporting Australian small businesses when they need it most.

The SME Recovery Loan Scheme builds on earlier loan schemes introduced during COVID‑19. Around 74,000 loans totalling around $6.2 billion were written.

The loans will be available through participating lenders until 31 December 2021. The expansion complements the Commonwealth’s other financial support to businesses impacted by the current COVID‑19 health restrictions.

The Morrison Government will continue to support small businesses as they seek to rebuild, adapt and create jobs on the other side of this crisis.

Further information can be found on the Treasury website.

AUSTRALIANS LOSE $70 MILLION ON SCAMS, ACCORDING TO SCAMWATCH

- There was a 119.6 per cent increase in the losses associated with investment scams between the first six months of 2020 compared with the first six months of 2021.

- Cryptocurrencies were the most common payment method used in investment scams and caused the biggest losses. Of the 1,931 reports involving a loss, 955 (49.5%) were due to cryptocurrencies with losses of $29,277,896. Bitcoin accounted for over $25 million of these losses.

- People aged 65 years and over have lost the most money to investment scams so far in 2021, experiencing losses of $18.8 million from 548 reports.

- There has been an increase of 66 per cent in the number of reports about investment scams made by people aged 18-24 years. The losses of more than $1.7 million so far is an increase of 259 per cent compared to all of last year.

- Indigenous consumers made 84 reports of investment scams and lost $945,270, a three-fold increase on the $336,796 lost for all of last year.

- The phone was the most common contact mode used with investment scams, accounting for 1,429 reports (30%) of all investment scam reports with losses of $27.7 million (39% of all losses to investment scams).

- Mobile apps and social networking sites accounted for 40% of all investment scams, which involved a financial loss.

GRANTS TO BOOST AUSTRALIAN EXPORTERS’ GLOBAL GROWTH

In August, Minister for Trade, Tourism, and Investment Dan Tehan outlined recent reforms to export grants. The grants will better support Australian exporters to succeed on the world stage, supporting local jobs and businesses.

Applications are now open for the reformed Export Market Development Grants (EMDG). The program has been improved by simplified legislation, a streamlined application process and a shift to a forward-looking grant program to ensure exporters know how much funding they will receive before they spend.

The EMDG program has helped support Australian success stories like the Wiggles, Atlassian and Penfolds to become international sensations.

Our Government provided $214.5 million to more than 4,700 Australian businesses to support their exporting activities through the EMDG program in 2020-21.

These businesses employed more than 70,000 people and generated around $4.7 billion in export income.

EMDG is a valuable form of assistance for Australian exporters. These changes will help many new and emerging exporters reach new heights in the years to come.

Since 1974 EMDG has supported close to 50,000 Australian exporters and distributed around $5.7 billion in grant payments.

The top five markets for EMDG grant recipients in 2020–21 were the US (56.9%), followed by the UK (25.3%), China (17.5%), Singapore (8.9%) and Canada (8.6%).

Reforms to EMDG are supported by a new application form which allows for better integration across Austrade services to deliver an improved client experience and export outcomes.

Applying for Export Market Development Grants from 1 July 2021

For export promotional activities from 1 July 2021, EMDG will no longer operate as a reimbursement scheme. Applications opened on 16 August and will close on 30 November 2021.

You can still claim reimbursement of eligible expenses incurred up to 30 June 2021 by applying under the final year of the reimbursement scheme. Applications for the reimbursement scheme close 30 November 2021 or 28 February 2022 if you are using a participating EMDG consultant.

The new forward-looking grant program will enable you to plan your marketing and promotional activities with confidence because you will know how much you will receive over the life of your grant agreement.

Grants are designed to support you during different stages of your export journey, and if you are an exporter or will be soon, you need to explore this.

CORPORATE TAX TRANSPARENCY DATA

The ATO publishes the tax details of large public and private companies every year in the Report of Entity Tax Information.

The ATO writes to the companies each September to check and, if needed, correct their information before they publish.

If you run or represent a large public or private company, you will receive a letter from the ATO soon. If you don’t receive a letter, you should contact the ATO.

The letter will list the details the ATO plan to publish to data.gov.au.

The ATO is legally required to publish information about corporate tax entities, that are:

- an Australian public or foreign-owned entity with a total income of $100 million or more

- an Australian resident private company with a total income of $200 million or more

- an entity reporting petroleum resource rent tax (PRRT) payable.

The information comes from their tax returns and includes the company:

- name

- Australian business number (ABN)

- total income

- taxable income

- total tax payable

- PRRT amount payable (if applicable)

The ATO will also publish details of 2017-18- and 2018-19-income tax returns if they were lodged or processed after 1 September 2020 and not published previously.

Published details could be taken from an entity’s original tax return or an entity-initiated amended assessment. The ATO does not publish the details of Commissioner-initiated amendments.

If your company or the company you represent meets the threshold for inclusion in the report and haven’t received a letter from the ATO by 4 October 2021, email ReportingEntityInfo@ato.gov.au.

You can also send general questions about the Annual Report of Entity Tax Information to this same mailbox.

STRENGTHENING UNFAIR CONTRACT TERM PROTECTIONS FOR CONSUMERS AND SMALL BUSINESSES

On 23.8.2021, the Government released an exposure draft Bill to strengthen Unfair Contract Term (UCT) protections for consumers and small businesses.

The Bill puts forward reforms to the Australian Consumer Law and the Australian Securities and Investments Commission Act 2001. These reforms help reduce unfair terms and improve consumer and small business confidence when entering into standard form contracts.

Key reforms include:

- prohibiting the use, application, and reliance on an unfair term

- providing courts with the power to impose a financial penalty for a contravention

- expanding the protections to capture a larger number of small businesses; and

- creating a rebuttable presumption that a term is unfair if a court has already found a similar term used in similar circumstances is unfair.

The consultation on the draft Bill follows an earlier consultation process on options to enhance the UCT protections.

TAX PLANNING OPPORTUNITIES WITH THE UNUSED SUPER CONTRIBUTIONS SPACE

Baby boomers are the envy of successive generations. Free education, security of employment, and superannuation concessions that were far more generous than now lead some to believe they have had a charmed life.

Many baby boomers (born between 1946 and 1960) have substantial amounts in superannuation and other assets.

They may have self-employed children who have not had the opportunity and/or the inclination to accumulate a significant amount in superannuation.

We have spoken in the past about the use of testamentary trusts in estate planning. The following strategy could also go part way to achieve a similar outcome with added tax benefits.

Whether we are dealing with a SMSF or managed funds… these are also funds in a trust. Since 1.7.2018, it has been possible to carry forward unused concessional super cap contributions for up to five years if your total superannuation fund balance is less than $500,000.

Consider Sam, who has a son Ian – who has worked as an independent building contractor his entire career and only has $200,000 in super.

Some builders flourished in these trying times, and for the year ended 30.6.2022, Ian will have a taxable income of $225,000. He has not made any superannuation for four years.

This means his unused concessional (tax deductible) cap balance is:

1.7.2018 – 30.6.2021 …. 3 x $25,000

1.7.2021 – 30.6.2022 …. $25,000

As a result, for the year ended 30.6.2022, Ian could make a tax-deductible contribution to superannuation for $102,500.

As part of his estate planning, his father Sam gifts Ian $102,500 to put into the fund, who is also very relieved to hear his tax bill for the year has been slashed by $43,575.

Mindful that the building industry has its commercial risks, Sam wants Ian to sharpen his focus on retirement saving and views superannuation as a secure haven (asset protection).

After a great outcome, Ian resolves to put funds aside each month as a direct debit into super.

Another scenario

Leaving aside the generous father, with the same unused super space, consider a case in a booming property market where Ian has sold an investment property for a taxable capital gain of $200,000.

He is told that as he has owned the property longer than 12 months, the capital gains tax individual 50% discount applies.

Capital gain $100,000

Less superannuation contributions $102,500

Net tax deduction ($2,500)

If we assume Ian is on the highest marginal tax, he has effectively lowered his tax bill by $48,175 while taking responsible measures to secure his retirement.

RE-CONTRIBUTION OF COVID-19 EARLY RELEASE SUPER AMOUNTS

On 3.8.2021, the ATO announced individuals can now re-contribute amounts they withdrew under the COVID-19 early release of super program without them counting towards their non-concessional contributions cap. These contributions can be made between 1 July 2021 and 30 June 2030.

COVID-19 re-contribution amounts are not a new type of contribution. They are a personal contribution that will be excluded from an individual’s non-concessional contribution cap.

Individuals can make COVID-19 re-contribution amounts to any fund of their choice where the fund rules allow.

What you need to do

Individuals can use the approved form from the ATO website to make a COVID-19 re-contribution. If you require assistance with this, contact us or the ATO. Superannuation funds may choose to design their own Notice of re-contribution of COVID-19 early release amounts approved form for members, as outlined in the CRT Alert 008/2021.

Once a super fund receives a completed approved form from their member, they need to:

- Check the COVID-19 re-contribution amount. An amount cannot be accepted where it exceeds $20,000. You may wish to confirm with your member if the correct figure has been provided.

- Provide the ATO with the information from the approved forms the fund received on a monthly basis – they are not required to provide nil lodgement reports.

There is no change for the superannuation fund when accepting and reporting personal contribution amounts that a member treats as a COD-1VI9 re-contribution.

There is further information on the ATO website.

ATO ISSUES GUIDANCE ON TAX DEDUCTIONS FOR NON-ASSESSABLE NON-EXEMPT (NANE) COVID-19 GRANTS

Recently the Federal Government declared a number of COVID-19 business support programs eligible for non-assessable non-exempt (NANE) income treatment.

Broadly, payments will be treated as NANE income if made under an eligible program, received in the current financial year, and received by a business with an aggregated turnover of less than $50 million.

The ATO has issued guidance making it clear you can only claim a tax deduction for the part of these expenses related to gaining your assessable income. You cannot claim a tax deduction for the part that relates to getting the non-taxable government grant.

There is no set way to work out the part of the expense that relates to each purpose, but the way you work it out should be fair and reasonable. You should keep a record of how you work it out.

Example – Expenses incurred to gain assessable income and to get a non-taxable government grant

Flame Pty Ltd is eligible to receive a non-taxable government grant.

Flame Pty Ltd asks their accountant to apply for this grant on their behalf. Their accountant does not separately bill Flame Pty Ltd for this service but itemises the fee charged for applying for the grant in a quarterly bill that they give to Flame Pty Ltd for professional services provided over the quarter.

Flame Pty Ltd cannot claim a deduction for this part of the Bill.

Expenses that you would usually incur in the ordinary course of carrying on your business but are incidentally related to getting a non-taxable government grant

You can claim a tax deduction for the whole of these expenses.

Getting a government grant is considered incidental where the expense relates to the whole of your business and is of a kind you would usually incur. The ATO will consider that a government grant is not incidental where the expense is not one that you usually incur and is a pre-condition of being eligible for the grant.

Example – Expenses incidentally related to getting a non-taxable government grant

Flame Pty Ltd is eligible for a non-taxable government grant if they keep their staff on the payroll.

Flame Pty Ltd uses the grant to pay for wages, rent and utilities that they would ordinarily incur in carrying on his business.

Flame Pty Ltd can claim a deduction for the wages, rent and utilities paid.

YOUR FUTURE, YOUR SUPER REFORMS REVEAL UNDERPERFORMING MYSUPER PRODUCTS

As part of the most significant changes to superannuation in nearly 30 years, the Federal Government is holding underperforming funds to account. They aim to strengthen protections for retirement savings.

The first annual performance test outcomes for MySuper products have been published in the online YourSuper comparison tool. Superannuation members can now access a single, trusted, and independent source of information to compare superannuation products, including whether they are in an underperforming product.

The first annual performance test revealed that $56.2 billion is invested in underperforming products, with these products holding almost 1.1 million accounts. The test assessed the performance of 76 MySuper products and found that 13 of these have underperformed.

Importantly, eight products have exited the market since the Government announced the performance test, demonstrating that the positive impact of the test extends beyond singling out underperforming funds.

Funds failing the test have until 27.9.2021 to notify members of their underperformance. They must provide them with details of the YourSuper comparison tool so they can consider whether a different product would better suit their needs.

The Australian Prudential Regulation Authority (APRA) has also written to superannuation funds whose products fail or marginally pass the performance test. The letter sets out their supervisory expectations and assesses the credibility of funds plans to improve their performance. Products that fail the annual performance test again next year will be closed to new members until their performance improves.

The Your Future, Your Super reforms are estimated to save Australian workers $17.9 billion over 10 years. Through these measures, the Government aims to ensure the superannuation system works harder for all Australians by increasing transparency and accountability of returns generated for members.

From next year, the annual performance test will also be expanded to a wider range of superannuation products, providing more members with the assurance that their product is being held to the highest standards of accountability.

Details on whether a MySuper product has passed the performance test are available on the YourSuper comparison tool.

ANTI-AVOIDANCE TASK FORCE FOCUS IN 2021–22

The ATO has outlined the Tax Avoidance Taskforce targets for 2021-22. During 2021–22, the focus will continue to be specialist large market advisors who promote and run tax avoidance schemes and engage in uncooperative, misleading, and obstructive behaviour.

This includes the misuse of legal professional privilege (LPP) during their reviews and audits. The ATO is developing best practice guidance to establish best practices when making LPP claims in a tax dispute.

Engagement and streamlined assurance programs will use growing data holdings to identify and treat tax avoidance behaviours. There will be continued engagement with the Top 500 and Next 5000 taxpayers and their associated entities.

Through their Medium and Emerging, and international programs, the ATO uses their growing data holdings to identify and treat tax avoidance behaviours. This data also improves the ATO’s system design to ensure leveraged approaches are applied across this population, reducing risk.

The Top 1000 Combined Assurance Review program commenced in late September 2020 and builds on the Top 1000 tax performance program. Work will commence with the reviews and associated engagements regarding those taxpayers that obtained overall low assurance.

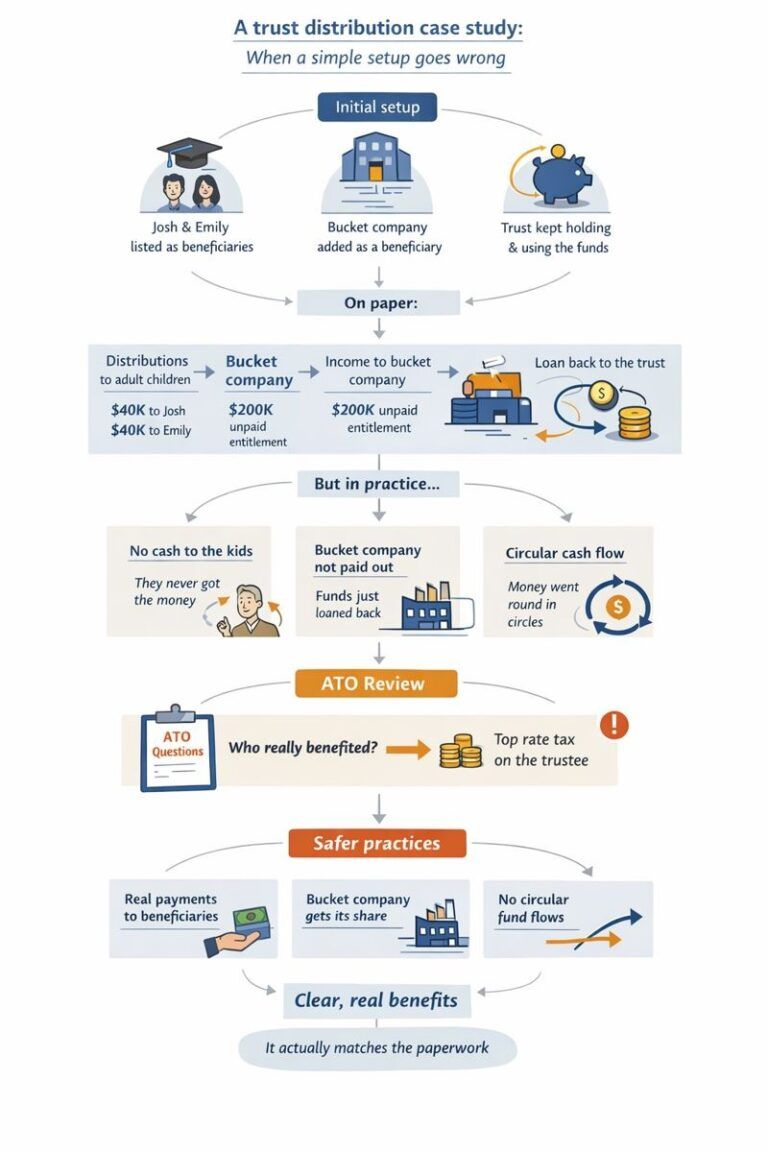

Complex trust structures and distribution flows designed to exploit the use of trusts will again be firmly in ATO sights.

The ATO is sharpening its focus on the small number of wealthy individuals (and their private groups) who engage in deliberate tax avoidance behaviours by working with their partner agencies to remove and disrupt harmful practices.

The ATO will continue to advance their D&A capabilities and use of cutting-edge technology to improve the way they analyse and use data to support the Taskforce. Further improvements to data accessibility and risk detection services will enhance their ability to target engagement and assurance work. This program of work will continue over the next two years, with technology and analytics enhancements that continue to manage, interrogate, and provide insights from their extensive data resources.