Practice Update October 2020

Ian Campbell • 5 October 2020

Federal Government to Adopt Us-Style Insolvency Rules to Help with Expected Wave of Business Closures

The Federal Government has announced it will overhaul insolvency rules, adopting an American-style model to help small businesses struggling because of the coronavirus pandemic to either restructure or fold.

The new system is two-tiered. Large companies will work under existing insolvency rules, while business with liabilities of less than $1 million will have access to a simpler system.

The changes would see small business owners remain in control of their company and assets, rather than immediately being placed in the hands of an administrator or creditors.

An insolvent small business will have 20 days to come up with a restructuring plan, and creditors would have to vote on whether to accept it within 15 days after that.

For small businesses that cannot be revived, liquidation would be changed, too, in an effort to make it quicker and easier.

The changes aim to limit liquidators’ investigative processes, mandatory meetings, and reporting requirements.

According to Treasurer Josh Frydenberg

- The changes will allow viable businesses to survive the recession caused by the COVID-19 pandemic.

- These are the most significant reforms to Australia’s insolvency framework in almost 30 years and will help to keep more businesses in business and Australians in jobs.

- The Government’s new reforms draw on key features of the US Chapter 11 bankruptcy process allowing small businesses to restructure their debts while remaining in control of their business.

Compared to 2019, the number of companies entering external administration is down 46%, with many unviable businesses being propped up by the Federal Government’s JobKeeper wage subsidies.

A criticism of the current system is that the cost of putting a business into administration or liquidation is so expensive that some small businesses find the process consumes all of their remaining assets.

The changes follow concerns in the financial sector, including regulatory bodies that many small businesses are putting off restructuring and incurring greater debt as a result.

- A wave of insolvencies is anticipated once emergency protections for business owners expire on 31.12.2020.

- These emergency provisions include limiting statutory demands by creditors, giving companies more time to respond to creditors’ demands and removing personal liability for trading whilst insolvent.

Similar emergency provisions for personal bankruptcy introduced in March also apply until the end of the year.

The Federal Government will also address concerns that there will not be enough insolvency practitioners to deal with the number of businesses that need to restructure or liquidate at the end of the year.

Several initiatives are proposed to encourage more professionals into the field, including waiving registration fees for two years and creating a new class of insolvency practitioners who will have their work limited to the simplified small business process.

Protections for small businesses will be introduced for those who announce they want to restructure but cannot get immediate access to an insolvency practitioner.

More details will follow in the Federal Budget to be handed down on 5.10.2020.

Extension of Temporary Relief for Financially Distressed Businesses

The Federal Government will continue its regulatory relief for businesses that have been impacted by the Coronavirus crisis by extending temporary insolvency and bankruptcy protections until 31 December 2020.

Regulations have been made to extend the temporary increase in the threshold at which creditors can issue a statutory demand on a company and the time companies have to respond to statutory demands they receive.

The changes also extend the temporary relief for directors from any personal liability for trading while insolvent.

These measures were part of more than 80 temporary regulatory changes the Government made designed to provide greater flexibility for businesses and individuals to operate during the coronavirus crisis.

The extension of these measures will lessen the threat of actions that could unnecessarily push businesses into insolvency and external administration at a time when they continue to be impacted by health restrictions.

These changes will help to prevent a further wave of failures before businesses have had the opportunity to recover.

As the economy starts to recover, it will be critical that distressed businesses have the necessary flexibility to restructure or to wind down their operations in an orderly manner.

Government policy is to continue to help businesses successfully adapt and restructure so that they can bounce back on the other side of this crisis.

Amendments to Fair Work Act Under JobKeeper 2.0

As part of the Federal Government’s Coronavirus Economic Response Package (Jobkeeper Payments) Amendment Bill 2020, new amendments have been made to the Fair Work Act 2009.

This creates two tiers of employers:

- Employers who meet (or continue to meet) the criteria to receive JobKeeper payments after 28 September 2020 (Qualifying Employers); and

- Employers who previously met the criteria under ‘JobKeeper 1.0’ to access JobKeeper payments, but who do not quality for such payments after 28 September 2020 (Legacy Employers)

For Qualifying Employers, the proposed amendments generally extend the existing rights and obligations that were available under ‘JobKeeper 1.0’ in relation to employees who receive JobKeeper payments (Eligible Employers), for the period until 29 March 2021 (with only minor modifications).

The general payment obligations for Qualifying Employers continue to apply, including that such employers much satisfy the ‘wage condition’ and must meet the ‘minimum payment guarantee’ for each Eligible Employee.

The new provisions for Legacy Employers stipulate they must hold a valid ’10 percent decline in turnover certificate’ (Deadline in Turnover Certificate), in order to be eligible to issue or seek JobKeeper enabling directions or agreements, at a particular time.

To hold this certificate, a Legacy Employer must satisfy the ’10 percent decline in turnover test’ for a quarter (relevantly, the 3-month periods ending on 30 June, 30 September, and 31 December). While adopting the definition used in the JobKeeper Rules, this test only requires a 10 percent reduction of projected GST turnover for the relevant period. Decline in Turnover Certificates must be issued :

- by an ‘eligible financial service provider’ (such as registered auditor, tax agent or accountant) who is not associated with the Legacy Employer (unless the Legacy Employer is a small business employer under the FW Act, in which case a statutory declaration can be made for the Legacy Employer); and

- for each relevant quarter. New Decline in Turnover Certificates are required to subsequent quarters.

There will be significant penalties for Legacy Employers who purport to give a JobKeeper enabling direction, if they do not satisfy the 10 percent decline in turnover test at the time the direction was given, and the Legacy Employer knew or was reckless to that fact. Penalties also apply for providing false or misleading information to an eligible financial service provider, for the purpose of obtaining a Decline in Turnover Certificate.

In addition, the Federal Court will have powers to terminate a JobKeeper enabling direction or agreement, if a Legacy Employer who holds a Decline in Turnover Certificate did not in fact satisfy the 10 percent decline in turnover test, at the particular time that the direction was issued or agreement was made.

JobKeeper enabling directions

Eligible Legacy Employers will be able to issue or seek certain JobKeeper enabling directions or agreements, however these will be in more limited form than for Qualifying Employers and subject to additional conditions. Employers should take advice in the key differences between the JobKeeper enabling directions available to Qualifying Employers and Legacy Employers.

Failure to Consult Renders Redundancy Non-Genuine

The Fair Work Commission recently ruled that an employer’s failure to consult and consider ways to avoid retrenchment rendered the redundancy non-genuine.

The FW Commissioner accepted that the role performed by the employee was no longer required to be filled by anyone because of changes in the company’s operational needs and therefore met the requirements of the Fair Work Act’s s389(1)(a).

As the company did not comply with the consultation obligations under the applicable award it meant the redundancy was not genuine as per the Act.

Many workplace disputes arise where there have been decisions and/or changes made which the employees are aggrieved about and will or may impact their duties or future with an organisation. Downsizing, restructuring, rightsizing, up skilling, multi-skilling, and demarcation are some of the main issues which give rise to disputes of this nature.

All modern awards include a consultation clause which seeks to reduce the likelihood of disputes where change occurs, and a consultation clause is required to be inserted in all enterprise agreements.

The use of this clause places onus on the employer to ensure that a consultation process is entered into to reduce the possibility of industrial unrest.

Consultation clauses must also include ‘genuine’ consultation with employees if there is a change to working hours or rosters. Employers will be required to notify employees, seek feedback on how these changes might affect them and consider the impact of these changes on staff.

In the case of a redundancy occurring it is important to follow the required consultative process and ensure that the following occurs:

- There isconsultation with the affected employees in accordance with the terms of any applicable award or enterprise agreement covering these employees.

- Consideration is given to the option of relocating or retraining the employees within the organisation and if this option exists, an offer is made to the affected employees.

- You meet the obligations of any affected employees who may be on parental leave by discussing and providing information on any relevant changes which may affect the position of the employee on parental leave.

- If their pre-parental leave position is going to be made redundant they are entitled to return to an available position that is closest to their pre-parental leave role, providing that a position is available and they are suitably trained and qualified to perform the duties of the alternate role.

- If the employee/’s position is to be made redundant, you ensure that the employee receives the appropriate redundancy payments either under the terms of the National Employment Standards (NES) or any applicable contract or company policy.

When determining the actual employees to be made redundant there are a number of recognised methods which are deemed to be acceptable by the relevant tribunals including:

- Seniority or ‘last on first off’ principle, although this method was once the standard practice it has now been recognised that this approach may give rise to age discrimination claims and it can also deplete the corporate knowledge of the business.

- Job performance: this method should be undertaken so that the poorest performing staff are made redundant to improve the overall efficiency of the organisation, but it must be handled carefully and be procedurally correct in its application.

- Potential: this method is where the employees identified to have the least potential are made redundant and requires the procedure to be handled carefully and be procedurally correct in its application.

- Voluntary redundancy: this method is widely used but can create expectations in the workforce and can also result in a mass exodus of the more experienced staff that are more likely to be able to find alternative employment.

Personal Services Income (PSI) Rules

Income is classified as PSI when more than 50% of the income received under a contract is for a taxpayer’s labour, skills, or expertise.

The personal services income rules are integrity provisions which ensure individuals cannot reduce or defer their income tax by diverting income for their personal services through companies, partnerships, or trusts. If the rules apply, the individual is taxed on the income directly.

The rules do not apply if at least 75% of the individual’s personal services income is for producing a result, where the individual supplies all the required “tools of trade” and is liable for rectifying defects in the work. This is known as the “results test”.

To pass the unrelated clients test your PSI must be produced from two or more clients who are not related or connected, and the work must be obtained by making offers to the public or sections of the public.

You pass the test in an income year if you meet both of the following conditions:

- Two or more unrelated clients

- Making offers to the public.

You do not pass the unrelated clients test if you source all your work through arrangements such as a labour hire firm.

If you operate through a company, partnership, or trust and you have more than one individual generating PSI, you will need to work out whether you pass the unrelated clients test for each individual. It is possible to be a PSB for one individual but not another.

Making offers to the public

To satisfy this condition, there must be a definite connection between the offer to the public at large and the engagement for the work.

Making offers to the public (or a section of the public) includes maintaining a website, applying for competitive public tenders, or advertising in a newspaper, industry journal or business directory.

The ATO maintains registering with labour hire firms or similar will not meet this condition.

SMSF Regulations to Allow Six Members Under New Legislation

In September, the Treasury Laws Amendment (Self-Managed Superannuation Funds) Bill 2020 was introduced.

This partially implements the measure to allow an increase in the maximum number of allowable members in self-managed superannuation funds and small APRA funds from four to six. The remainder of the measure will be implemented through regulations. These measures were first mentioned in the May 2018 Federal Budget.

The bill amends the SIS Act, Corporations Act, ITAA1997 to increase members in SMSFs. It also amends provisions that relate to SMSFs and small APRA funds, which will ensure continued alignment with the increased maximum number of members for SMSFs.

SMSFs are often used by families as a vehicle for controlling their own superannuation savings and investment strategies. For larger families, the only real option is to create two SMSFs – in so doing incurring additional costs.

The key differences are shown in the comparison table below and is also detailed in the explanatory memorandum.

New law

A superannuation fund can only be an SMSF if it has no more than six (6) members.

Various provisions that apply to small superannuation funds apply to funds with no more than six (6) members.

Current law

A superannuation fund can only be an SMSF if it has fewer than five (5) members.

Various provisions that apply to small superannuation funds apply to funds with fewer than five (5) members.

In some instances, the number of individual trustees that a trust can have may be limited to less than five or six trustees by state legislation and could prevent some or all members of a fund with five or six members from being individual trustees. In these cases, the members of a fund should use a corporate trustee in order for the superannuation fund to meet, or continue to meet, the amended definition of an SMSF.

Under the updated requirements, a SMSF with one or two directors or individual trustees must have its accounts and statements signed by all of those directors or trustees. For all other SMSFs with between three and six directors or trustees, the accounts, and statements of the SMSF will have to be signed by at least half of the directors or individual trustees.

Legislation Passes Through the Senate to Allow Australians to Choose Their Superannuation Fund

Legislation giving Australians the power to choose their own superannuation fund, instead of being forced into a fund because of enterprise bargaining agreements passed the Senate on 25.8.2020.

The Treasury Laws Amendment (Your Superannuation, Your Choice) Bill 2019 will allow around 800,000 Australians to make choices about where their hard-earned retirement savings are invested, representing around 40 per cent of all employees covered by a current enterprise agreement.

The Bill addresses the findings of the Financial System Inquiry and the Productivity Commission Inquiry into the efficiency and competitiveness of the superannuation system which found that this reform was ‘much needed’ and that denying choice of fund can discourage member engagement and lead to them paying higher fees.

This reform is also supported by a recent decision of the Fair Work Commission which found that it was detrimental to employees to restrict them from being able to choose their own superannuation fund. Specifically, the Fair Work Commission determined that extending choice of fund to employees who were previously denied choice will prevent them from unnecessarily ending up with multiple superannuation accounts “with all the inconvenience and additional administration costs that this involves”.

These changes also build on the Government’s earlier reforms which protect superannuation accounts from being eroded through the capping of fees on low balance accounts and requiring insurance to be provided on an opt-in basis for new members under 25 years of age.

With around 16 million Australians having a superannuation account and around $2.9 trillion worth of superannuation savings, the Government maintains it will continue to ensure that the superannuation system is delivering for all Australians.

Changing Business Structures

Many small businesses change their business structure from a sole trader to more complex company or trust structures, especially when the environment changes. This can lead to errors.

Some of the common errors identified by the ATO include:

- reporting income for the wrong entity

- claiming expenses incurred by another entity as business expenses

- personal use of business bank accounts.

- the company is a separate legal entity from them as a shareholder or director

- money that the company earns, belongs to the company

- the company owns its assets, and they cannot treat them as their own

- if a director or shareholder of a company uses company assets for their personal use, it must be properly treated as a benefit to the director or shareholder. The Division 7A or fringe benefits tax (FBT) provisions could apply if not treated correctly.

If you move to a trust structure, be mindful of a trustee’s responsibilities, including:

- holding the trust property (including assets, investments, and income) for the benefit of the beneficiaries

- managing the trust’s tax affairs

- paying some tax liabilities.

You should also consider the small business restructure rollover when thinking about restructuring

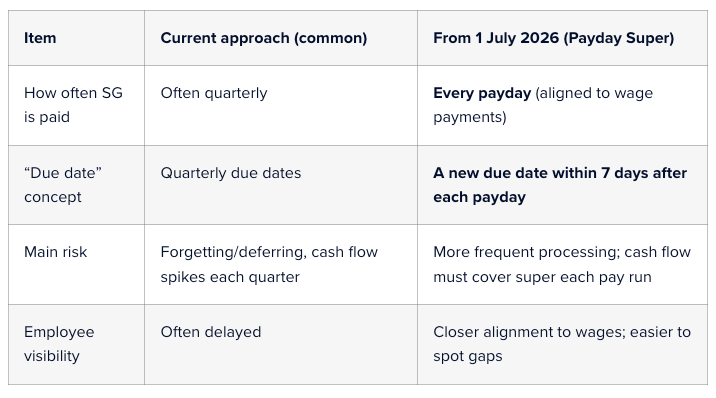

Cashflow red flags for small business in 2026

Readiness strategies in preparation for the Payday Super If you run a small business, paying Superannuation can feel like “one more admin job” on top of payroll, BAS and everything else. Two key changes mean Superannuation deserves a fresh look this year: The Super Guarantee (SG) rate is 12% for 1 July 2025 to 30 June 2026 (and remains 12% after that). From 1 July 2026, “Payday Super” starts — employers will be required to pay SG on payday , rather than quarterly, and contributions must be paid into the employee’s fund within 7 days of payday . What does SG at 12% mean in everyday terms? SG is calculated on an employee’s Ordinary Time Earnings (OTE) (often the base rate and ordinary hours, plus certain loadings/allowances depending on how they’re paid). The key point for most businesses is that the Superannuation cost is now 12 cents for every $1 of OTE. If you haven’t already, it’s worth confirming whether your staff packages are “plus super” (super on top) or “inclusive of super” (rare, but it happens). A small misunderstanding here can quietly create underpayments. What is “Payday Super” and why is it changing? Many employers pay the Superannuation Guarantee (SG) quarterly. Payday Super changes the rhythm: From 1 July 2026 , each time you pay OTE to an employee, it creates a new super payment obligation for that payday. You’ll have a 7-day due date for the SG to arrive in the employee’s fund after each payday (this is designed to allow time for payment processing). The ATO is implementing the change, and guidance is already being published to help employers prepare. This reform is aimed at reducing unpaid super and making it easier for workers to see whether super has actually been paid, closer to when they’re paid wages. Quarterly vs payday Super

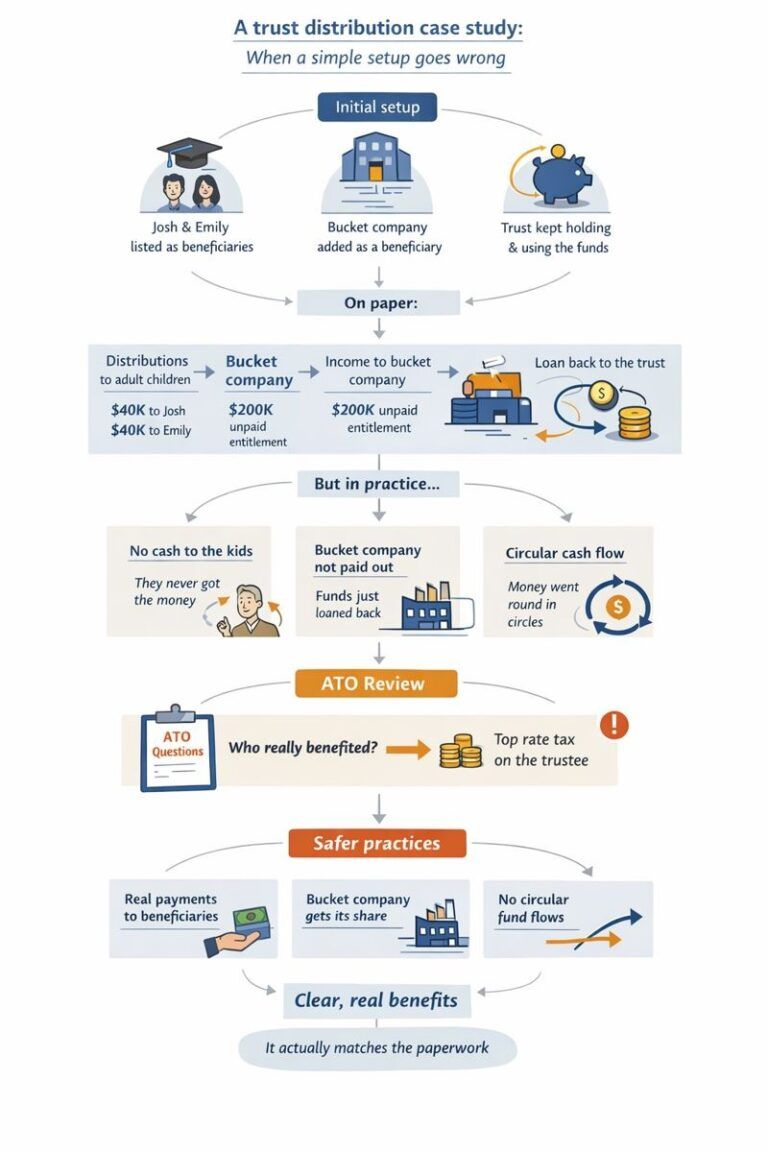

A real-world case study on trust distributions Mark and Lisa had what most people would describe as a “pretty standard” setup. They ran a successful family business through a discretionary trust. The trust had been in place for years, established when the business was small and cash was tight. Over time, the business grew, profits improved, and the trust started distributing decent amounts of income each year. The tax returns were lodged. Nobody had ever had a problem with the ATO. So naturally, they assumed everything was fine. This is where the story starts to get interesting. Year one: the harmless decision In a good year, the business made about $280,000. It was suggested that some income be distributed to Mark and Lisa’s two adult children, Josh and Emily. Both were over 18, both were studying, and neither earned much income. On paper, it made sense. Josh received $40,000. Emily received $40,000. The rest was split between Mark, Lisa, and a company beneficiary. The tax bill went down. Everyone was happy. But here’s the first quiet detail that mattered later. Josh and Emily never actually received the money. No bank transfer. No separate accounts. No conversations about what they wanted to do with it. The trust kept the funds in its main business account and used them to pay suppliers and reduce debt. At the time, nobody thought twice. “It’s still family money.” “They can access it if they need it.” “We’ll square it up later.” These are very common thoughts. And this is exactly where risk quietly begins. Year two: things get a little more complicated The next year was even better. They used a bucket company to cap tax at the company rate. Again, a common and legitimate strategy when used properly. So the trust distributed $200,000 to the company. No cash moved. It was recorded as an unpaid present entitlement. The idea was that the company would get paid later, when cash flow allowed. Meanwhile, the trust needed funds to buy new equipment and cover a short-term cash squeeze. The trust borrowed money from the company. There was a loan agreement. Interest was charged. Everything looked tidy on paper. From the outside, it all seemed sensible. But economically, nothing really changed. The trust made money. The trust kept using the money. The same people controlled everything. The bucket company never actually used the funds for its own business or investments. This detail becomes important later. Year three: circular money without anyone realising By year three, things had become routine. Distributions were made to the kids again. The bucket company received another entitlement. Loans were adjusted at year-end through journal entries. What is really happening is a circular flow. Money was being allocated to beneficiaries, then effectively coming back to the trust, either because it was never paid out or because it was loaned back almost immediately. No one was trying to hide anything. No one thought they were doing the wrong thing. They were just following what they’d always done. This is how section 100A issues usually arise. Slowly, quietly, and without any single dramatic mistake.