Practice Update January 2021

Ian Campbell • 12 January 2021

JOBKEEPER KEY DATES AND ACTIONS FOR EMPLOYERS

- 4 January 2021 – the JobKeeper extension 2 starts and the payment rates change for your eligible employees – see payment rates.

- Between 4 January 2021 and 28 January 2021 – complete the December business monthly declaration (this is an extension of two weeks past the usual due date of the 14th day of each month).

- By 31 January 2021 – new entities enrolling for JobKeeper will need to enrol and submit their ‘Check decline in turnover’ form to the ATO online – see actual decline in turnover test.

- 31 January 2021 – for JobKeeper fortnights 21 and 22 only (from 4 January 2021 and 18 January respectively 2021), the ATO is allowing employers until 31 January 2021 to pay their employees (meet the wage condition).

- The sooner you complete and submit your decline in turnover and business monthly declaration, the sooner the ATO can process your JobKeeper payment.

PROPOSED CHANGES TO FRINGE BENEFITS TAX RECORD-KEEPING

The government has proposed that it will provide the Commissioner of Taxation with the power to allow employers to rely on alternative records, such as existing corporate records where adequate to finalise their fringe benefits tax (FBT) returns. This would be an alternative to employee declarations and other prescribed records.

If enacted the change will have effect from the start of the first FBT year (1 April) after the date of royal assent of the legislation, which cannot be earlier than 1 April 2021.

JOBKEEPER UPDATE

On 30.11.2020, the Federal Government released preliminary data on JobKeeper 2.

Announced in March 2020, the first phase of JobKeeper supported more than 3.6 million workers and around 1 million businesses, with payments totalling nearly $70 billion for the 13 JobKeeper fortnights to 27 September 2020.

Following a re-test of business eligibility for the second phase of JobKeeper, for the two JobKeeper fortnights in October, around 500,000 entities have had applications processed covering more than 1.5 million employees/eligible business participants (ATO data, current as at 26 November 2020).

The preliminary data indicates that around 450,000 fewer businesses and around 2 million fewer employees qualified for JobKeeper in October than in September.

Around 86 per cent of workers qualified for the Tier 1 payment of $1,200 per fortnight, with around 14 per cent on the Tier 2 payment of $750 per fortnight.

These preliminary October JobKeeper figures suggest an improvement on the 2020-21 Budget assumption of 2.2 million recipients for the December quarter, with around 700,000 fewer employees/eligible business participants covered by the Payment in October due to their employer no longer meeting the required decline in turnover test.

The lower-than-forecast take-up of the JobKeeper Payment extension in October is further evidence that Australia’s recovery from this once-in-a-century pandemic is well underway.

Recent economic data shows that outside Victoria, employment has recovered to be less than one per cent below March levels with some 650,000 jobs created in the past five months nationwide.

These are encouraging numbers.

HOMEBUILDER SUCCESS SEES PROGRAM EXTENDED

The Federal Government has extended HomeBuilder programme which is driving demand in the construction sector by supporting the construction on new homes and home renovations.

HomeBuilder will remain demand driven and will be extended from 1 January 2021 to 31 March 2021 which is expected to support the construction or major rebuild of around 15,000 homes. This is in addition to the 27,000 homes the scheme is already expected to support, bringing it to a total of around 42,000 homes across Australia.

According to Prime Minister Scott Morrison and Treasurer Josh Frydenberg:

- HomeBuilder is a key part of my government’s Economic Recovery Plan for Australia. We are keeping people in jobs and putting Australians’ dream homes within reach.

- It is critical we keep the momentum up for Australia’s economic recovery.

- Extending HomeBuilder will mean a steady pipeline of construction activity to keep tradies on the tools.

- The Homebuilder program has delivered the stimulus the housing sector needed.

- The sector is worth $100 billion dollars a year to the Australian economy or around 5 per cent of GDP and more than a million people are employed in the sector across Australia.

- The success of this program has not only meant an increase in work on the ground to keep the pipeline of construction flowing but it has also protected jobs in the construction sector as well as across the economy.

HomeBuilder has been adjusted for the building and housing market’s conditions, and after consultation with the construction sector.

For all new build contracts signed between 1 January 2021 and 31 March 2021:

- Eligible owner-occupier purchasers will receive a $15,000 HomeBuilder: and

- The property price caps for new builds in New South Wales and Victoria will be increased to $950,000 and $850,000, respectively.

Up until 29.11.2020, data showed HomeBuilder had already had around 24,000 applications, on track to exceed expected take up levels.

This announcement also builds upon the extension of the First Home Loan Deposit Scheme announced in the Budget, which delivered 10,000 guaranteed loans to allow first home buyers to obtain a loan to build a new home, or purchase a newly built home, with a deposit of as little as five per cent.

LEGITIMATE BUSINESS BAILOUT OR RISKY PHOENIXING?

On 26.11.2020, the ATO warned business advisers about inappropriate dealings with pre-insolvency advisers. The ATO is aware that in today’s challenging economic conditions some advisers’ business clients may seek advice on whether to pause, change or permanently close their business.

While the vast majority of advisers do the right thing, some untrustworthy or unqualified advisers may offer inappropriate pre-insolvency advice to their clients. This advice may include illegal phoenix activity, and recommendations to remove their client’s assets before closing their business, for use in a copy of the original business.

Clients should check they are seeking or receiving advice from qualified professionals, such as an accountant, lawyer, registered liquidator, or a registered trustee. They need to be wary of some of the common red flags of untrustworthy advisers, including:

- cold calling with offers of advice

- unsolicited correspondence after court action by a creditor

- advice to transfer assets to a third party without payment

- refusal to provide advice in writing

- suggestions they have a sympathetic liquidator who will protect your client’s personal interests/assets

- advising that certain records be withheld from the bankruptcy trustee or liquidator

- suggestions they deal with the liquidator/trustee on your behalf.

The ATO is firmly of the view that if a client needs to wind up their company, they should be referred to a registered liquidator or registered trustee.

AN ADVERSE ACTION AND BREACH OF CONTRACT CLAIM ($5.2 MIL) THAT ALL EMPLOYERS SHOULD KNOW ABOUT

The Federal Court recently delivered a landmark judgment in a general protection claim, ordering an ASX-listed software company to pay more than $5.2 million in compensation, damages, and penalties to its former State Manager.

Employers take note…. This case involved claims that a manager was dismissed after making numerous complaints that he was bullied by senior executives.

This case highlights the importance of properly addressing bullying complaints and undertaking workplace investigations where appropriate, particularly prior to planning to terminate employment and where bullying allegations have been raised by that employee. The manner in which such complaints should be addressed will of course depend on the individual circumstances. The case also demonstrates how liability in general protections complaints can extend to an Executive team personally, and most notably, CEOs when they are the decision-maker.

What are the facts?

The applicant, we will call him BR, worked as the Victorian state manager for the software company, the first responder in this case. When BR commenced employment in July 2006, the company was relatively small. However, over time it grew significantly in terms of operations and revenue.

By way of illustration, BR’s gross income in 2006/2007 was $208,932 and increased in the 2015/16 financial year to $845,128 (most of the remuneration increase was connected to incentive payments). BR performed well during his employment and he was granted share options which was something not granted to any other state manager. He also received the distinct honour of receiving the Chairman’s Award.

BR filed a general protections compliant under the Fair Work Act 2009 (the Act) claiming that he was dismissed for prohibited reasons including seven instances of exercising his workplace rights by making complaints, in particular, to having been bullied.

The second respondent in the case was the executive chairman and CEO of the software company (the CEO). The Court found the CEO was the sole decision maker in the matter of terminating BR and that he twice rejected professional HR advice that it would be unfair to dismiss BR on the basis of his complaints, outlined further below.

From late 2010, BR was experiencing problems in his personal life. He sought to “escape his pain in work”, according to the Court decision, and increased his already extensive working hours as a result.

Subsequently, BR allegedly experienced bullying from senior executives at the software company in the form of having his role and responsibilities undermined, having his position threatened, and being verbally abused and sworn at in front of his colleagues.

Between February 2016 and May 2016, BR made seven different complaints to four different people, including the CEO, relating to these instances of bullying.

On 18 May 2016, BR’s employment was terminated summarily. The reason given by the CEO for BR’s termination was, among other things, that he was unable to get along with his previous three managers, that concerns had been raised by BR’s team and that revenue in Victoria (for which BR was responsible) was not growing.

What does the law say?

BR claimed he was dismissed for prohibited reasons, contrary to the general protection provision in the Fair Work Act. His claims were, among other things, that:

- he had exercised his workplace rights by making complaints of having been bullied by his managers

- he had proposed to exercise the workplace right to bring legal proceedings under a workplace law (the Fair Work Act)

- he had proposed to exercise his contractual safety net, being the right to receive incentive payments in respect of certain company products sold in Victoria and that he was entitled to receive those payments

In summary BR’s claim arose primarily from two sections of the Fair Work Act, being:

- section 340 – provides that an employee is protected from having adverse action taken against them, merely for having or exercising a workplace right.

- section 341 – provides a wide definition of what constitutes and gives rise to a ‘workplace right’. That is a benefit, role or responsibility under a workplace related law, instrument, process or proceeding, and explicitly includes employees who make complaints relating to their employment.

The Court found that the software company’s ‘Open Door Policy’ (meaning all managers are capable of hearing employee complaints) and its ‘Workplace Bullying Policy’ applied throughout BR’s employment. This provided an explicit basis for the Court to be satisfied that BR was “able to make a complaint… about his having been bullied in relation to his employment”.

Accordingly, the Court found that BR was protected from adverse action arising from the making of his complaints.

In concluding its lengthy judgment, the Court also found that BR’s seven complaints, made between February and May 2016, were a “substantial and operative factor” in the CEO’s reasons to terminate his employment. This was a breach of section 340 of the Fair Work Act, as described above.

The Court also found that the sole decision maker responsible for terminating BR was the software company’s CEO, and that the CEO was fully aware of the bullying allegations when terminating BR’s employment. The Court decided that the CEO chose the interests of BR’s alleged bullies over the interests of BR and terminated his employment unlawfully.The Court formulated that if the CEO had taken the advice of HR and undertaken an investigation, this would likely have led to consideration of the conduct of senior staff members, including HR, and that any formal investigation would risk uncovering issues which the CEO would prefer not to explore.

What is the damage?

As a result of all this, the Court ordered penalties and damages in excess of $5,200,000. BR was awarded $2,825,000 for his future economic loss, representing over four years of future losses (less incentive payments he would not have received, and the Court applied a 15% discount to factors which may have affected his earning capacity), $756,410 to compensate for share options, $1,590,000 in damages for breach of contract and $10,000 in general damages for pain and suffering.

This pay out amount may actually be a new record for this type of case in the Fair Work Division of the Federal Court.

The Court also fined the CEO personally the sum of $7,000 and the software company $40,000 for their breaches of the Act and both fines were paid directly to BR. It is worth noting that the Court made this order to achieve ‘effective deterrence’ and that CEOs in similar positions should resist the temptation “to stand with the bullies rather than the bullied”.

Points to remember

All employers should be mindful of the reputational damage that may be suffered for failing to take appropriate steps to comply with the Fair Work Act.

The decision maker must be able to, if need be, refute the claims that the decision was in breach of a workplace right. In other words, the decision maker must be able to demonstrate that the decision was not made for a prohibited reason.

Significant damages may be awarded against employers, and senior executives, if they are found to have acted because of a prohibited reason and in breach of an employee’s workplace right under the Fair Work Act.

However, whilst this case should alert employers to the risks of adverse action taken for prohibited reasons, large awards like the one in this case are rare. This case can be distinguished on its facts due to the employee’s undisclosed depressive disorder making him incapable of work again, the rejection of HR advice by the CEO, and the seniority and earning capacity of the employee.

The software company has said that it plans to appeal against the decision and has “always believed that it has acted lawfully”.

OECD UPGRADES AUSTRALIA’S ECONOMIC GROWTH OUTLOOK

In its latest Economic Outlook Report, the Organisation for Economic Co-operation and Development (OECD) has upgraded Australia’s economic growth outlook for 2020 while noting that “the COVID-19 pandemic continues to exert a substantial toll on economies and societies”.

According to the OECD, global GDP will contract by 4.2 per cent in 2020, before picking up by 4 1⁄4 per cent in 2021. The OECD says there is “now hope for a brighter future” with vaccines in sight however “the recovery will be uneven across countries, potentially leading to lasting changes in the world economy”.

The OECD has upgraded its outlook for the Australian economy by 0.3 percentage points following the Federal Budget released on 6 October. The OECD now expects Australia’s economy to contract by 3.8 per cent in 2020 (previously 4.1 per cent). This compares favourably to an average fall of 5.5 per cent across all advanced economies.

These figures are despite Victoria’s “strict state-wide” lockdown measures which the OECD recognised led to an “interstate divergence in consumer sentiment and labour market outcomes”.

The OECD also emphasised the Morrison Government’s economic response to the COVID-19 pandemic, pointing to JobKeeper as having “covered nearly one million employers and one-third of all employment, containing the rise in the measured unemployment rate so far”.

This finding was recently confirmed by research from the Reserve Bank of Australia (RBA) which found that the temporary payment helped to reduce “total employment losses by at least 700,000”.

In addition to the effectiveness of JobKeeper, the OECD notes the importance of the Government’s Economic Recovery Plan, in particular personal income tax cuts, the JobMaker Hiring Credit and planned insolvency reforms which it describes as “key”.

These changes are the most significant to Australia’s insolvency framework in 30 years, drawing on features of the Chapter 11 bankruptcy model in the United States, ultimately keeping businesses in business and Australians in jobs.

The Economic Recovery Plan outlined in the 2020-21 Budget designed to help create more jobs, boost our economy recovery, and secure Australia’s future.

RETIREMENT INCOME REVIEW FINAL REPORT

On 20.11.2020, the Federal Government released the independent Retirement Income Review Final Report which confirms that “the Australian retirement income system is effective, sound and its costs are broadly sustainable.”

The Review also finds that Australia’s retirement income system is well placed to respond to the economic challenges posed by the COVID-19 pandemic.

The Review was recommended by the Productivity Commission in its report Superannuation: Assessing Efficiency and Competitiveness and comes 27 years after the establishment of compulsory superannuation.

The Review makes three over-arching observations about the system. Firstly, that the three pillars of the existing retirement income system, being the Age Pension, compulsory superannuation, and voluntary savings, continue to provide effective support to Australian retirees and are sustainable in the long term.

Secondly that there is a need to improve understanding of the system so that all Australians can make the most of their assets in retirement. Thirdly, that the system would benefit from a clear objective in order to guide future policy and provide a framework for assessing its performance.

The Final Report also makes a number of key observations with respect to each of the system’s three pillars, including:

- The Age Pension, compulsory superannuation and voluntary savings results in most Australians achieving adequate retirement outcomes.

- The Age Pension provides a strong safety net to those who retire with small superannuation balances.

- The Age Pension reduces income inequality among retirees, as low-income retirees receive the largest Age Pension payments.

- Superannuation assists middle income earners to smooth their income over their lives. Without compulsory superannuation, middle income earners would not save enough for retirement.

- More efficient use of savings in retirement can have a bigger impact on improving retirement income than increasing the Superannuation Guarantee (SG).

- The weight of evidence suggests an increase in the SG rate will result in lower wages growth, impacting standards of living.

- There are a number of ways that individuals can significantly boost their retirement incomes without having to increase their superannuation contributions, including more effectively drawing on superannuation assets, achieving better-after-fee returns and accessing equity in their home.

- Voluntary contributions provide flexibility for those outside the compulsory system to contribute to superannuation, such as the self-employed and those who have had interrupted working careers.

- The Government’s early release policy, enabling Australians to access up to $20,000 of their superannuation across two years, has cushioned the economic impact of COVID-19.

Through its work, the review has established a fact base that will improve understanding of how the retirement income system operates, better informing public policy and the retirement outcomes delivered to Australians.

Importantly, the Review provides confirmation of the policy direction being pursued by the Morrison Government with respect to the importance of increasing the efficiency of the superannuation system and lifting home ownership rates – both identified as key drivers of an adequate retirement income.

Specifically, the Government’s ‘Your Future, Your Super’ reforms will simplify and enhance member engagement with their superannuation and increase the efficiency of the superannuation system through lowering fees and improving returns, benefiting Australians by $17.9 billion over the next 10 years.

Additionally, given the importance of home ownership to the financial security and wellbeing of Australians in retirement, the Government will continue to support measures to allow more Australians to buy their first home sooner, including through our First Home Loan Deposit Scheme, First Home Super Saver Scheme and HomeBuilder.

The Government will continue to carefully consider the observations made in the Review together with the findings of related reviews including the Aged Care Royal Commission and remaining recommendations of the Productivity Commission’s report into Superannuation.

The focus of the media coverage on the report was on whether the staggered legislated increases to the superannuation guarantee to 12% would now take place. While the economic and fiscal arguments will play out in 2021, it is considered likely the proposed increases will now be scrapped and that the superannuation guarantee will remain at 9.5%.

DOCUMENTATION IS ESSENTIAL FOR SUCCESSFUL R&D CLAIMS

Royal Wins Pty Ltd and Innovation and Science Australia (ISA) [2020] AATA 4320

This recent Administrative Appeals Tribunal’s (AAT) decision demonstrates the importance of taxpayers appropriately documenting a hypothesis prior to the commencement of research and development (R&D) activities.

The hypothesis must have an element of uncertainty that is formulated for the purposes of being validated or invalidated through the process of experiments. Clearly documentation for R&D must be contemporaneous, following a systematic progression of work in order to satisfy the legislative criteria. Relevant expert evidence should also be obtained in order to argue the case. If the AAT is only presented with evidence from one expert that unopposed evidence, is likely to be accepted.

This case involved the taxpayer’s entitlement to have certain activities registered as core or supporting R&D activities for the purposes of the Tax Act. Deputy President Molloy found in favour of Innovation and Science Australia (ISA) on the basis that due to the lack of adequate documentation, he was unable to determine what work was done, when it was done, that Royal Wins had started with a hypothesis or that it had undertaken a systematic progression of work based on the principles of established science.

For those contemplating R&D activities, reading the judgement online will confirm the importance of complying with the requirements of legislation and properly documenting the research activities each step of the way.

This of course all needs to be carefully planned prior to the commencement of activities.

All too often either advisers or participants decide it is a good idea to access the R&D tax incentives well after activities have commenced. This can be problematic.

How to structure business-income to build wealth

Cashflow red flags for small business in 2026

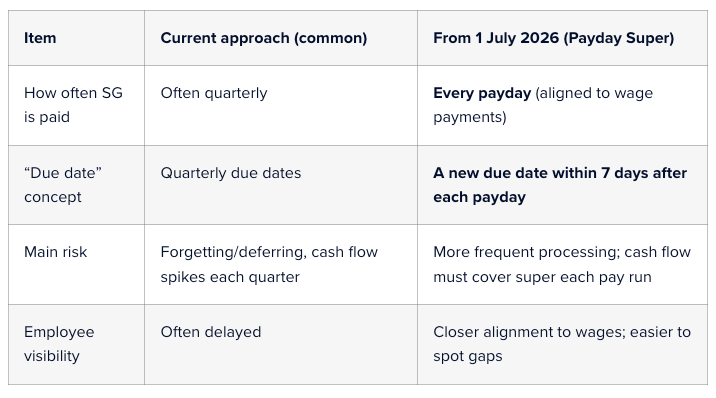

Readiness strategies in preparation for the Payday Super If you run a small business, paying Superannuation can feel like “one more admin job” on top of payroll, BAS and everything else. Two key changes mean Superannuation deserves a fresh look this year: The Super Guarantee (SG) rate is 12% for 1 July 2025 to 30 June 2026 (and remains 12% after that). From 1 July 2026, “Payday Super” starts — employers will be required to pay SG on payday , rather than quarterly, and contributions must be paid into the employee’s fund within 7 days of payday . What does SG at 12% mean in everyday terms? SG is calculated on an employee’s Ordinary Time Earnings (OTE) (often the base rate and ordinary hours, plus certain loadings/allowances depending on how they’re paid). The key point for most businesses is that the Superannuation cost is now 12 cents for every $1 of OTE. If you haven’t already, it’s worth confirming whether your staff packages are “plus super” (super on top) or “inclusive of super” (rare, but it happens). A small misunderstanding here can quietly create underpayments. What is “Payday Super” and why is it changing? Many employers pay the Superannuation Guarantee (SG) quarterly. Payday Super changes the rhythm: From 1 July 2026 , each time you pay OTE to an employee, it creates a new super payment obligation for that payday. You’ll have a 7-day due date for the SG to arrive in the employee’s fund after each payday (this is designed to allow time for payment processing). The ATO is implementing the change, and guidance is already being published to help employers prepare. This reform is aimed at reducing unpaid super and making it easier for workers to see whether super has actually been paid, closer to when they’re paid wages. Quarterly vs payday Super