2020 Economic Stimulus Package

23 March 2020

ECONOMIC STIMULUS PACKAGE (COVID-19)

On 12.3.2020, the Federal Government announced a $17.6 billion economic plan to keep Australians in jobs, keep businesses in business and support households and the Australian economy as the world deals with the significant challenges posed by the spread of the coronavirus.

The targeted stimulus package is focused on keeping Australians in jobs and helping small and medium sized businesses to stay in business.

The package has four parts:

Supporting business investment

Providing cash flow assistance to help small and medium sized business to stay in business and keep their employees in jobs

Targeted support for the most severely affected sectors, regions and communities;

Household stimulus payments that will benefit the wider economy

According to Prime Minister Scott Morrison the measures are all temporary, targeted and proportionate to the challenge we face.

The actions will ensure we respond to the immediate challenges we face and help Australia bounce back stronger on the other side, without undermining the structural integrity of the Budget.

As part of the plan up to 6.5 million individuals and 3.5 million businesses would be directly supported by the package.

Delivering support for business investment

$700 million to increase the instant asset write off threshold from $30,000 to $150,000 and expand access to include businesses with aggregated annual turnover of less than $500 million (up from $50 million) until 30 June 2020. For example, assets that may be able to be immediately written off are a concrete tank for a builder, a tractor for a farming business, and a truck for a delivery business.

$3.2 billion to back business investment by providing a time limited 15 month investment incentive (through to 30 June 2021) to support business investment and economic growth over the short term, by accelerating depreciation deductions. Businesses with a turnover of less than $500 million will be able to deduct an additional 50 per cent of the asset cost in the year of purchase.

These measures commenced on 12.3.2020 and will support over 3.5 million businesses (over 99 per cent of businesses) employing more than 9.7 million employees or 3 in every 4 workers. The measures are designed to support business sticking with investment they had planned, and encouraging them to bring investment forward to support economic growth over the short term.

Cash flow assistance for businesses

$6.7 billion to Boost Cash Flow for Employers by up to $25,000 with a minimum payment of $2,000 for eligible small and medium-sized businesses. The payment will provide cash flow support to businesses with a turnover of less than $50 million that employ staff, between 1 January 2020 and 30 June 2020. The payment will be tax free. This measure will benefit around 690,000 businesses employing around 7.8 million people. Businesses will receive a credit of 50% of the tax withheld in their activity statement from 28 April with refunds to be paid within 14 days.

$1.3 billion to support small businesses to support the jobs of around 120,000 apprentices and trainees. Eligible employers can apply for a wage subsidy of 50 per cent of the apprentice’s or trainee’s wage for up to 9 months from 1 January 2020 to 30 September 2020. Where a small business is not able to retain an apprentice, the subsidy will be available to a new employer that employs that apprentice.

Stimulus payments to households to support growth

$4.8 billion to provide a one-off $750 stimulus payment to pensioners, social security, veteran and other income support recipients and eligible concession card holders. Around half of those that will benefit are pensioners. The payment will be tax free and will not count as income for Social Security, Farm Household Allowance and Veteran payments. There will be one payment per eligible recipient. If a person qualifies for the one off payment in multiple ways, they will only receive one payment.

Payments will be from 31 March 2020 on a progressive basis, with over 90 per cent of payments expected to be made by mid-April.

Assistance for severely-affected regions

$1 billion to support those sectors, regions and communities that have been disproportionately affected by the economic impacts of the Coronavirus, including those heavily reliant on industries such as tourism, agriculture and education. This will include the waiver of fees and charges for tourism businesses that operate in the Great Barrier Reef Marine Park and Commonwealth National Parks. It will also include additional assistance to help businesses identify alternative export markets or supply chains. Targeted measures will also be developed to further promote domestic tourism. Further plans and measures to support recovery will be designed and delivered in partnership with the affected industries and communities.

The Government is also offering administrative relief for certain tax obligations, including deferring tax payments up to four months. This is similar to relief provided following the bushfires for taxpayers affected by the coronavirus, on a case-by-case basis. The ATO will set up a temporary shop front in Cairns within the next few weeks with dedicated staff specialising in assisting small business. In addition, the ATO will consider ways to enhance its presence in other significantly affected regions to make it easier for people to apply for relief, including considering further temporary shop fronts and face-to-face options.

The Government maintains its economic support package is proportionate, timely and scalable to respond to the economic challenges presented by the spread of the coronavirus.

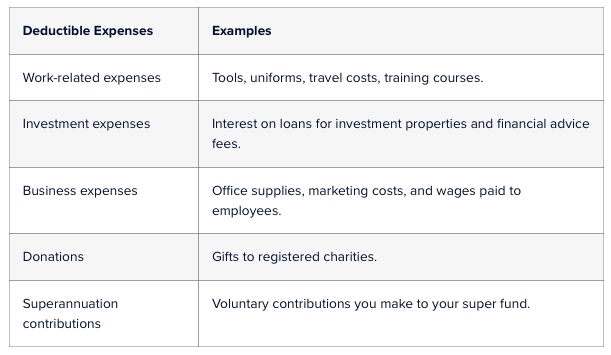

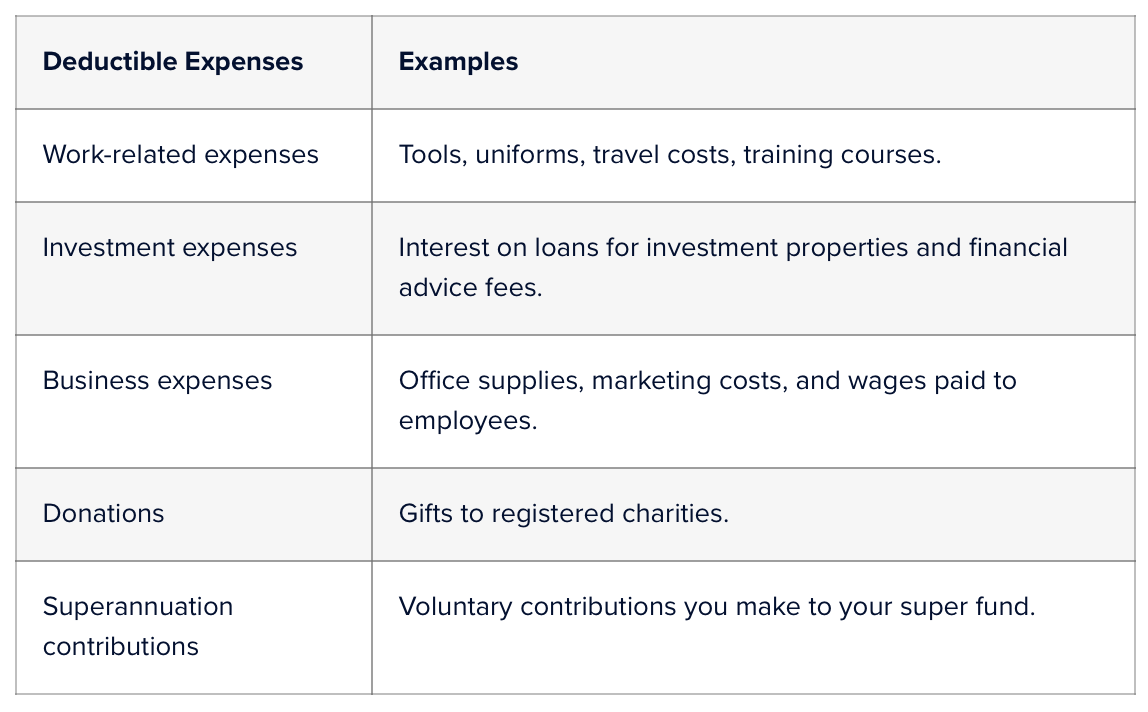

Strategies for individuals before June 30, 2025

Strategies for individuals before June 30, 2025

A foreign entrepreneur’s guide to starting a business in Australia Starting a business as a foreign entrepreneur can be an exhilarating way to access new markets, diversify investment portfolios, and create fresh opportunities. Many countries around the globe provide pathways for non-residents and foreign nationals to register businesses. However, understanding different countries’ legal requirements, procedures, and opportunities is crucial for success. In this issue, we will navigate the process of establishing a business in Australia to help foreign entrepreneurs looking to register a company in Australia. Key takeaways Foreign entrepreneurs can fully own Australian businesses with no restrictions on ownership. Registered office and resident director requirements are key legal considerations. ABN and ACN are essential for business registration. The application process can be done online, simplifying the process for foreign entrepreneurs. Why register a business as a foreign entrepreneur? There are various reasons why a foreigner may want to register a company in another country. These reasons include expanding into a foreign market, taking advantage of favourable tax laws, leveraging local resources, or benefiting from business-friendly regulatory environments. Before registering, conducting thorough market research to assess whether establishing a business abroad aligns with your objectives is essential. Understanding the country’s political and economic climate, legal framework, and tax system will help ensure the success of your venture. The general process for registering a business as a foreign entrepreneur While the exact requirements may differ from country to country, some common steps apply to most jurisdictions when registering a company as a foreign entrepreneur: Choosing the business structure The first step is deciding on the appropriate business structure. The structure determines liability, taxation, and governance. Common types of business structure include: Sole proprietorship: A single-owner business where the entrepreneur has complete control and entire liability. Limited Liability Company (LLC): Offers liability protection to the owners, meaning their assets are not at risk. Corporation (Inc.): A more complex structure that can issue shares and offers limited liability to its shareholders. Different countries have varying rules regarding foreign ownership, so understanding the options available is essential before registering a company. Registering with local authorities Regardless of the jurisdiction, most countries require you to register your company with the relevant local authorities. This process typically includes submitting documents such as: Company name and business activities: You need to choose a unique company name that adheres to local naming regulations. Articles of incorporation: This document outlines the company’s structure, activities, and bylaws. Proof of identity : As a foreign entrepreneur, you will likely need to provide a passport and other identification documents. Proof of address: Many countries require a physical address for the business, which may be the address of a registered agent or office. Tax Identification Number (TIN) and bank accounts After registering the company, you will typically need to apply for a tax identification number (TIN), employer identification number (EIN), or equivalent, depending on the jurisdiction. This number is used for tax filing and reporting purposes. Opening a business bank account is another critical step. Some countries require a local bank account for business transactions, and you may need to visit the bank in person or appoint a local representative to help with the process. Complying with local regulations Depending on the type of business, specific licenses and permits may be required to operate legally. For example, food service, healthcare, or transportation companies may need specific licenses. Compliance with local labour laws and intellectual property protections may also be necessary. Appoint directors and shareholders To register a company, you’ll need to appoint at least one director who resides in Australia. The director will be responsible for ensuring the company meets its legal obligations. You will also need to appoint shareholders, who can be either individuals or corporations. For foreign entrepreneurs, the requirement for a resident director is one of the key challenges. If you don’t have a trusted individual in Australia to act as the director, you can engage a professional service to fulfil this role. This ensures your business remains compliant with local regulations. Choose a company name Next, you need to choose a company name. The name should reflect your business but must be unique and available for registration. You can check the availability of a name through the Australian Securities & Investments Commission (ASIC) website. Remember that the name must meet legal requirements and cannot be similar to an existing registered company. If you’re unsure, seeking professional advice is always a good move. Apply for an Australian Business Number (ABN) and Australian Company Number (ACN) Once you’ve selected your business structure and appointed your directors, it’s time to apply for an Australian Business Number (ABN) and an Australian Company Number (ACN). These are essential for running your business in Australia. ABN: This unique 11-digit number allows your business to interact with the Australian Taxation Office (ATO) and other government agencies. ACN: This 9-digit number is allocated to your company upon registration with ASIC and serves as your business’s unique identifier. You can easily apply for both numbers online through the Australian Business Register (ABR) and the ASIC websites. Register for Goods and Services Tax (GST) If your business expects to earn more than $75,000 in revenue annually, you must register for GST. This means your business will charge customers an additional 10% on goods and services. The GST registration threshold for non-profit organisations is higher at $150,000 annually. If your company is below these thresholds, registering for GST is optional, but registration becomes mandatory once it exceeds the limit. Set up a registered office Every Australian company must have a registered office in Australia. This is where all official government documents, including legal notices, are sent. You can use your premises or hire a foreign company registration service to provide a virtual office address. Common challenges for foreign entrepreneurs While the process is relatively simple, there are a few hurdles that foreign entrepreneurs may encounter when registering a company in Australia: Resident director requirement: You’ll need a director residing in Australia. If you don’t have one, you’ll need to engage a service provider to fulfil this role. Understanding local tax laws: Australia has a corporate tax rate of 25% for small businesses with annual turnovers of less than $50 million. However, larger companies with turnovers exceeding $50 million are subject to a standard corporate tax rate of 30%. Foreign entrepreneurs must also understand the implications of the Goods and Services Tax (GST) and payroll tax. Compliance with Australian regulations: Navigating Australia’s various regulations and compliance requirements can be time-consuming. An accountant or adviser can help you in this regard. FAQs Can I register a company in Australia as a foreigner? Yes, foreign entrepreneurs can register a company in Australia. The only requirement is to have a resident director. Do I need to be in Australia to register a company? No, you can complete the registration process online. However, you must appoint a resident director. Do I need an Australian bank account to start a business in Australia? You will need an Australian bank account to handle your business’s finances and transactions. Can I operate my Australian company from abroad? Yes, you can operate your company remotely, but you must comply with all local tax laws and regulations.