Practice Updates

BUDGET 2026-27 BUDGET 2026-27 AT A GLANCE

How to structure business-income to build wealth

Cashflow red flags for small business in 2026

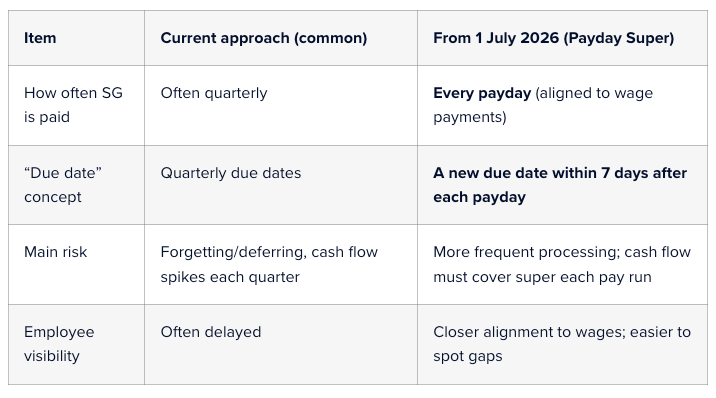

Readiness strategies in preparation for the Payday Super If you run a small business, paying Superannuation can feel like “one more admin job” on top of payroll, BAS and everything else. Two key changes mean Superannuation deserves a fresh look this year: The Super Guarantee (SG) rate is 12% for 1 July 2025 to 30 June 2026 (and remains 12% after that). From 1 July 2026, “Payday Super” starts — employers will be required to pay SG on payday , rather than quarterly, and contributions must be paid into the employee’s fund within 7 days of payday . What does SG at 12% mean in everyday terms? SG is calculated on an employee’s Ordinary Time Earnings (OTE) (often the base rate and ordinary hours, plus certain loadings/allowances depending on how they’re paid). The key point for most businesses is that the Superannuation cost is now 12 cents for every $1 of OTE. If you haven’t already, it’s worth confirming whether your staff packages are “plus super” (super on top) or “inclusive of super” (rare, but it happens). A small misunderstanding here can quietly create underpayments. What is “Payday Super” and why is it changing? Many employers pay the Superannuation Guarantee (SG) quarterly. Payday Super changes the rhythm: From 1 July 2026 , each time you pay OTE to an employee, it creates a new super payment obligation for that payday. You’ll have a 7-day due date for the SG to arrive in the employee’s fund after each payday (this is designed to allow time for payment processing). The ATO is implementing the change, and guidance is already being published to help employers prepare. This reform is aimed at reducing unpaid super and making it easier for workers to see whether super has actually been paid, closer to when they’re paid wages. Quarterly vs payday Super

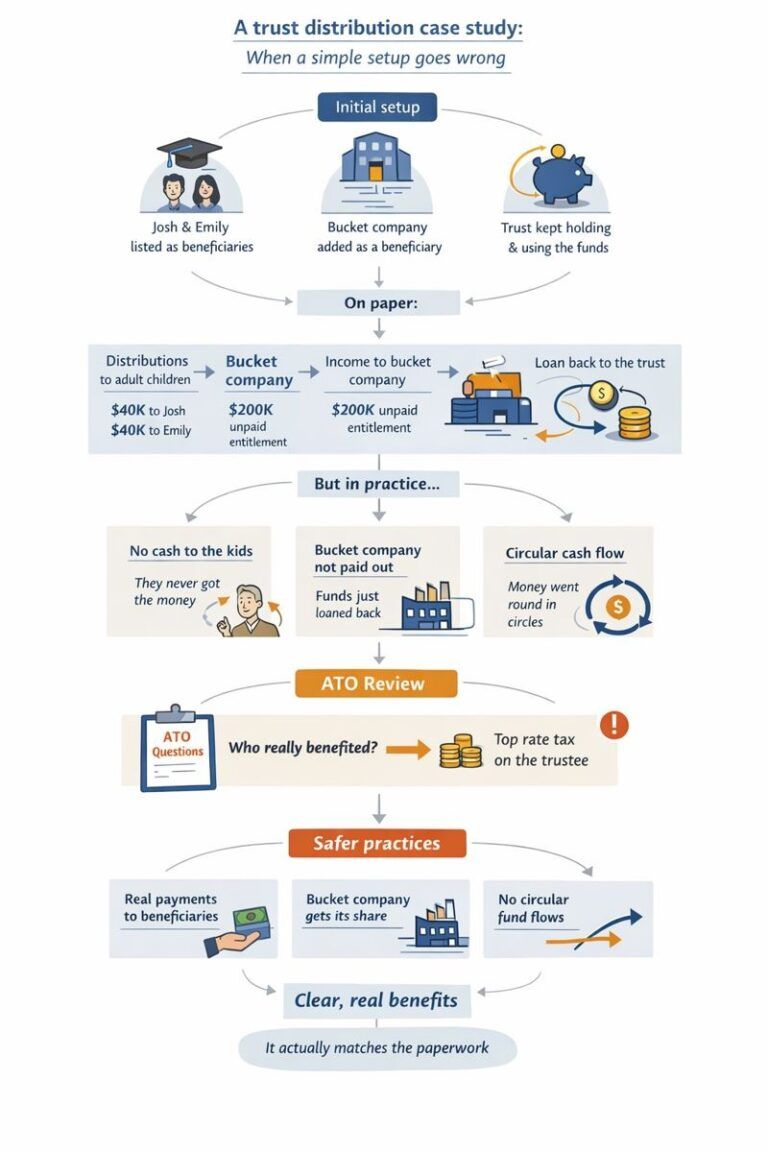

A real-world case study on trust distributions Mark and Lisa had what most people would describe as a “pretty standard” setup. They ran a successful family business through a discretionary trust. The trust had been in place for years, established when the business was small and cash was tight. Over time, the business grew, profits improved, and the trust started distributing decent amounts of income each year. The tax returns were lodged. Nobody had ever had a problem with the ATO. So naturally, they assumed everything was fine. This is where the story starts to get interesting. Year one: the harmless decision In a good year, the business made about $280,000. It was suggested that some income be distributed to Mark and Lisa’s two adult children, Josh and Emily. Both were over 18, both were studying, and neither earned much income. On paper, it made sense. Josh received $40,000. Emily received $40,000. The rest was split between Mark, Lisa, and a company beneficiary. The tax bill went down. Everyone was happy. But here’s the first quiet detail that mattered later. Josh and Emily never actually received the money. No bank transfer. No separate accounts. No conversations about what they wanted to do with it. The trust kept the funds in its main business account and used them to pay suppliers and reduce debt. At the time, nobody thought twice. “It’s still family money.” “They can access it if they need it.” “We’ll square it up later.” These are very common thoughts. And this is exactly where risk quietly begins. Year two: things get a little more complicated The next year was even better. They used a bucket company to cap tax at the company rate. Again, a common and legitimate strategy when used properly. So the trust distributed $200,000 to the company. No cash moved. It was recorded as an unpaid present entitlement. The idea was that the company would get paid later, when cash flow allowed. Meanwhile, the trust needed funds to buy new equipment and cover a short-term cash squeeze. The trust borrowed money from the company. There was a loan agreement. Interest was charged. Everything looked tidy on paper. From the outside, it all seemed sensible. But economically, nothing really changed. The trust made money. The trust kept using the money. The same people controlled everything. The bucket company never actually used the funds for its own business or investments. This detail becomes important later. Year three: circular money without anyone realising By year three, things had become routine. Distributions were made to the kids again. The bucket company received another entitlement. Loans were adjusted at year-end through journal entries. What is really happening is a circular flow. Money was being allocated to beneficiaries, then effectively coming back to the trust, either because it was never paid out or because it was loaned back almost immediately. No one was trying to hide anything. No one thought they were doing the wrong thing. They were just following what they’d always done. This is how section 100A issues usually arise. Slowly, quietly, and without any single dramatic mistake.

Rental deductions maximisation strategies

A Practical Guide to Running Your Family Business in Australia

TI scams in Australia: how to spot them and stay safe

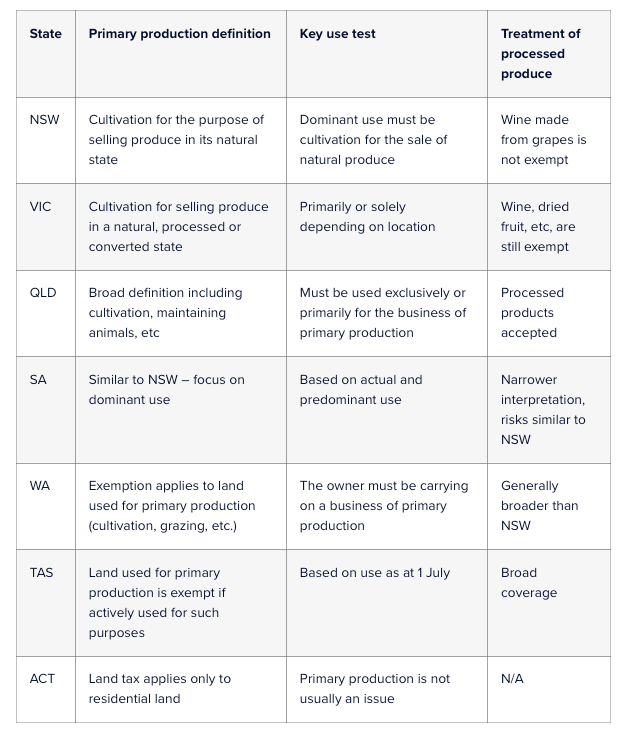

Land tax in Australia: exemptions, tips and lessons Land tax is one of those quiet state-based taxes that does not grab headlines like income tax or GST, but impacts property owners once thresholds are crossed. It applies when the unimproved value of land exceeds a certain amount, which differs from state to state. Principal places of residence are usually exempt, but investment properties, commercial holdings, and certain rural blocks may be subject to taxation. For individuals and small businesses, land tax is worth paying attention to because exemptions can make the difference between a manageable annual bill and a nasty surprise. A recent case in New South Wales (Zonadi case ) has sharpened the focus on when land used for cultivation qualifies for the primary production exemption. The lessons are timely for farmers, winegrowers and anyone with mixed-use rural land. The basics of land tax Each state and territory (except the Northern Territory) imposes land tax. Key features include: Assessment date : Usually determined at midnight on 31 December of the preceding year (for example, the 2026 assessment is based on ownership and use as at 31 December 2025). Thresholds : Vary across jurisdictions. For example, in 2025, the NSW threshold is $1,075,000, while in Victoria it is $300,000. Exemptions : Principal place of residence, primary production land, land owned by charities and specific concessional categories. Rates : Progressive, with higher landholdings paying higher rates. Unlike council rates, which fund local services, land tax is a revenue measure for states. It is payable annually and calculated on the total taxable value of landholdings. Primary production exemption Most states exempt land used for primary production from land tax. The policy aim is precise: farmers should not be burdened with land tax when using their land to produce food, fibre or similar goods. However, the details of what constitutes primary production vary. Qualifying uses generally include: cultivation (growing crops or horticulture) maintaining animals (grazing, dairying, poultry, etc.) commercial fishing and aquaculture beekeeping Sounds straightforward, but the catch is in how the land is used and for what purpose. Lessons from the Zonadi case The Zonadi case involved an 11-hectare vineyard in the Hunter Valley. The land was used for: 4.2ha of vines producing wine grapes a cellar door and wine storage area a residence and tourist accommodation some trees, paddocks and access ways During five land tax years in dispute, the taxpayer sold some grapes directly but used most of the crop to make wine off-site, which was then sold through the cellar door. Income was derived from grape sales, wine sales and tourist accommodation. The NSW Tribunal had to decide whether the land’s dominant use was cultivation for the purpose of selling the produce of that cultivation (a requirement under section 10AA of the NSW Land Tax Management Act). The outcome was a blow for the taxpayer. The Tribunal said: Growing grapes was indeed a form of cultivation and amounted to primary production. But cultivation for the purpose of making wine did not qualify, because the exemption only applies where the produce is sold in its natural state. Wine is a converted product, not the product of cultivation. Although some grapes were sold directly, the bulk of the financial gain came from wine sales. Therefore, the dominant use of the land was cultivation to make and sell wine, which is not exempt. The exemption was denied, and the taxpayer was left with a land tax bill. Why this matters For small businesses, especially those that combine farming with value-adding activities such as processing or tourism, the case serves as a warning. The line between primary production and secondary production can determine whether a land tax exemption applies. If most income comes from a cellar door, farmstay, or product manufacturing, the exemption may be at risk, even though cultivation is occurring on the land. Different rules in Victoria Victoria takes a broader view. It defines primary production to include cultivation for the purpose of selling the produce in a natural, processed or converted state. In other words, grapes sold for wine production would still be considered primary production. The only further hurdle is the “use test”, which depends on location: outside Greater Melbourne: land must be used primarily for primary production within urban zones: land must be used solely or mainly for the business of primary production Had Zonadi been in Victoria, the outcome could have been very different. The vineyard would likely have been exempt from this requirement. State-based comparisons Here’s a snapshot of how land tax treatment differs across states when it comes to cultivation and primary production:

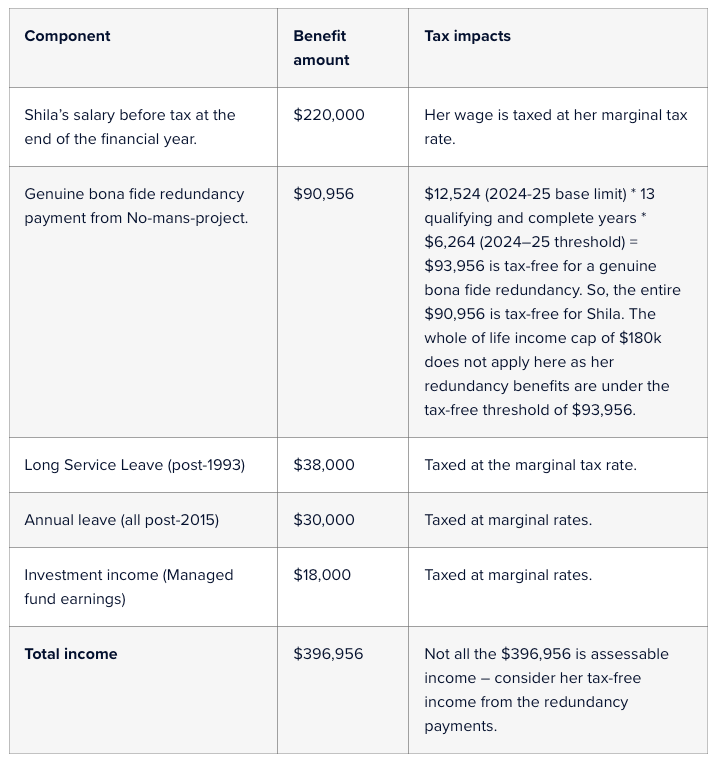

Shila is taking the leap

Key concerns when selling a business in: A strategic guide for business owners

Strategies for individuals before June 30, 2025

Strategies for individuals before June 30, 2025

A foreign entrepreneur’s guide to starting a business in Australia Starting a business as a foreign entrepreneur can be an exhilarating way to access new markets, diversify investment portfolios, and create fresh opportunities. Many countries around the globe provide pathways for non-residents and foreign nationals to register businesses. However, understanding different countries’ legal requirements, procedures, and opportunities is crucial for success. In this issue, we will navigate the process of establishing a business in Australia to help foreign entrepreneurs looking to register a company in Australia. Key takeaways Foreign entrepreneurs can fully own Australian businesses with no restrictions on ownership. Registered office and resident director requirements are key legal considerations. ABN and ACN are essential for business registration. The application process can be done online, simplifying the process for foreign entrepreneurs. Why register a business as a foreign entrepreneur? There are various reasons why a foreigner may want to register a company in another country. These reasons include expanding into a foreign market, taking advantage of favourable tax laws, leveraging local resources, or benefiting from business-friendly regulatory environments. Before registering, conducting thorough market research to assess whether establishing a business abroad aligns with your objectives is essential. Understanding the country’s political and economic climate, legal framework, and tax system will help ensure the success of your venture. The general process for registering a business as a foreign entrepreneur While the exact requirements may differ from country to country, some common steps apply to most jurisdictions when registering a company as a foreign entrepreneur: Choosing the business structure The first step is deciding on the appropriate business structure. The structure determines liability, taxation, and governance. Common types of business structure include: Sole proprietorship: A single-owner business where the entrepreneur has complete control and entire liability. Limited Liability Company (LLC): Offers liability protection to the owners, meaning their assets are not at risk. Corporation (Inc.): A more complex structure that can issue shares and offers limited liability to its shareholders. Different countries have varying rules regarding foreign ownership, so understanding the options available is essential before registering a company. Registering with local authorities Regardless of the jurisdiction, most countries require you to register your company with the relevant local authorities. This process typically includes submitting documents such as: Company name and business activities: You need to choose a unique company name that adheres to local naming regulations. Articles of incorporation: This document outlines the company’s structure, activities, and bylaws. Proof of identity : As a foreign entrepreneur, you will likely need to provide a passport and other identification documents. Proof of address: Many countries require a physical address for the business, which may be the address of a registered agent or office. Tax Identification Number (TIN) and bank accounts After registering the company, you will typically need to apply for a tax identification number (TIN), employer identification number (EIN), or equivalent, depending on the jurisdiction. This number is used for tax filing and reporting purposes. Opening a business bank account is another critical step. Some countries require a local bank account for business transactions, and you may need to visit the bank in person or appoint a local representative to help with the process. Complying with local regulations Depending on the type of business, specific licenses and permits may be required to operate legally. For example, food service, healthcare, or transportation companies may need specific licenses. Compliance with local labour laws and intellectual property protections may also be necessary. Appoint directors and shareholders To register a company, you’ll need to appoint at least one director who resides in Australia. The director will be responsible for ensuring the company meets its legal obligations. You will also need to appoint shareholders, who can be either individuals or corporations. For foreign entrepreneurs, the requirement for a resident director is one of the key challenges. If you don’t have a trusted individual in Australia to act as the director, you can engage a professional service to fulfil this role. This ensures your business remains compliant with local regulations. Choose a company name Next, you need to choose a company name. The name should reflect your business but must be unique and available for registration. You can check the availability of a name through the Australian Securities & Investments Commission (ASIC) website. Remember that the name must meet legal requirements and cannot be similar to an existing registered company. If you’re unsure, seeking professional advice is always a good move. Apply for an Australian Business Number (ABN) and Australian Company Number (ACN) Once you’ve selected your business structure and appointed your directors, it’s time to apply for an Australian Business Number (ABN) and an Australian Company Number (ACN). These are essential for running your business in Australia. ABN: This unique 11-digit number allows your business to interact with the Australian Taxation Office (ATO) and other government agencies. ACN: This 9-digit number is allocated to your company upon registration with ASIC and serves as your business’s unique identifier. You can easily apply for both numbers online through the Australian Business Register (ABR) and the ASIC websites. Register for Goods and Services Tax (GST) If your business expects to earn more than $75,000 in revenue annually, you must register for GST. This means your business will charge customers an additional 10% on goods and services. The GST registration threshold for non-profit organisations is higher at $150,000 annually. If your company is below these thresholds, registering for GST is optional, but registration becomes mandatory once it exceeds the limit. Set up a registered office Every Australian company must have a registered office in Australia. This is where all official government documents, including legal notices, are sent. You can use your premises or hire a foreign company registration service to provide a virtual office address. Common challenges for foreign entrepreneurs While the process is relatively simple, there are a few hurdles that foreign entrepreneurs may encounter when registering a company in Australia: Resident director requirement: You’ll need a director residing in Australia. If you don’t have one, you’ll need to engage a service provider to fulfil this role. Understanding local tax laws: Australia has a corporate tax rate of 25% for small businesses with annual turnovers of less than $50 million. However, larger companies with turnovers exceeding $50 million are subject to a standard corporate tax rate of 30%. Foreign entrepreneurs must also understand the implications of the Goods and Services Tax (GST) and payroll tax. Compliance with Australian regulations: Navigating Australia’s various regulations and compliance requirements can be time-consuming. An accountant or adviser can help you in this regard. FAQs Can I register a company in Australia as a foreigner? Yes, foreign entrepreneurs can register a company in Australia. The only requirement is to have a resident director. Do I need to be in Australia to register a company? No, you can complete the registration process online. However, you must appoint a resident director. Do I need an Australian bank account to start a business in Australia? You will need an Australian bank account to handle your business’s finances and transactions. Can I operate my Australian company from abroad? Yes, you can operate your company remotely, but you must comply with all local tax laws and regulations.

Do bucket companies help build wealth at retirement? Bucket companies are familiar with wealth-building strategies, particularly as individuals approach retirement. By distributing profits to a bucket company, individuals can benefit from reduced tax liabilities and enhanced investment growth opportunities. This essay explores how bucket companies influence wealth building at retirement, their impact on age pension eligibility and tax positions, and strategies to maximise economic outcomes. Understanding bucket companies A bucket company is used to receive distributions from a family trust. Instead of distributing profits directly to individuals, which may attract high marginal tax rates, the trust distributes income to the bucket company, which is taxed at the corporate tax rate (currently 30% or 25% for base rate entities). The company can then retain the after-tax profits for reinvestment or distribution. Impact on wealth building at retirement Tax efficiency and compounding growth Using a bucket company can result in significant tax savings compared to personal marginal tax rates, reaching up to 47% (including the Medicare levy). Retained earnings within the bucket company are taxed lower, allowing more capital to compound over time. Example of Tax Efficiency: Income DistributedPersonal Marginal Tax (47%)Bucket Company Tax (25%)Savings $100,000$47,000$25,000$22,000 Over 20 years, if the tax savings of $22,000 per year are reinvested at an annual return of 7%, they would accumulate to approximately $1,012,000. Age pension and means testing The age pension is subject to both an income test and an assets test. Holding wealth in a bucket company can impact these tests: Income Test: Distributions to individuals count as assessable income. Retained profits within the company do not. Assets Test: The value of the bucket company shares is counted as an asset, which may affect pension eligibility. Strategic use of the company can help individuals control their assessable income, potentially increasing their age pension entitlement. Strategies to maximise economic outcomes Timing of Distributions By deferring distributions from the bucket company until retirement, individuals can benefit from lower marginal tax rates or effectively use franking credits. Dividend Streaming Using franking credits from company-paid tax can reduce personal tax liabilities when distributed dividends. Investment within the Company Reinvesting retained earnings within the bucket company in diversified assets can enhance compounding returns. Family Trust Distribution Planning Strategically distributing income to lower-income family members before reaching the bucket company can reduce overall tax. Winding Up or Selling the Company Carefully planning an exit strategy to wind up the b ucket company or sell its assets can minimise capital gains tax liabilities. Example of a retirement strategy with a bucket company Assume that John and Mary, aged 65, have distributed $100,000 annually from their family trust to their bucket company over 20 years. Corporate tax paid: 25% Annual return on reinvestment: 7% After-tax reinvested earnings annually: $75,000 YearAnnual ReinvestmentTotal Accumulated Amount (7% p.a.)5$75,000$435,30010$75,000$1,068,91420$75,000$3,867,854 At retirement, they can distribute dividends with franking credits to minimise personal tax and supplement their income while potentially qualifying for some age pension benefits due to strategic income timing. FAQ What is a bucket company? A bucket company is a corporate entity that receives trust distributions, taxed at the corporate rate rather than personal marginal rates. How does a bucket company impact my age pension eligibility? While retained earnings do not affect the income test, the value of the company shares is considered an asset under the assets test. Can bucket companies help reduce tax during retirement? Yes, by using franking credits and strategic distribution timing, bucket companies can minimise tax liabilities. Are there risks associated with using bucket companies for retirement planning? Yes, risks include changes in tax laws, corporate compliance costs, and potential capital gains tax upon winding up the company. Should I consult a professional before using a bucket company? Absolutely. Professional advice is essential to ensure compliance with tax laws and optimise wealth-building strategies.

Personal super contribution and deductions

Don’t let taxes dampen your holiday spirit! Just like Santa carefully checks who’s naughty or nice, businesses need to watch the tax rules when spreading Christmas cheer. Hosting festive parties for employees or clients can lead to Fringe Benefits Tax (FBT). FBT is a tax employers pay when they provide extra perks to employees, their families, or associates. It’s separate from regular income tax and is based on the value of the benefit. The FBT year runs from 1 April to 31 March, and businesses must calculate and report any FBT they owe. With a bit of planning—just like Santa’s perfect delivery route—you can celebrate while keeping your tax worries in check! FBT exemption: A little Christmas gift from the taxman The tax rules include a “minor benefit exemption”—like a small stocking stuffer. If the benefit given to each employee costs less than $300 and isn’t a regular thing, it’s exempt from Fringe Benefits Tax (FBT). Christmas parties fit perfectly here because they’re one-off events. Businesses can avoid FBT hassles if the cost per employee stays under $300. Remember: the more often you give out perks, the less likely they’ll qualify for this exemption. Thankfully, Christmas only comes once a year! Christmas parties at the office If you host your Christmas party at your business premises during a regular workday, costs like food and drinks are FBT-free, no matter how much you spend. However, you can’t claim a tax deduction or GST credits for those expenses. If employees’ family members join and the cost per person is under $300, there’s still no FBT, but again, no tax deduction or GST credits can be claimed. However, FBT will apply if the cost is over $300 per person. The good news is that you can claim both a tax deduction and GST credits in that case. FBT check for Christmas parties at the office Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Employees onlyUnlimitedNoNoEmployees and their familyLess than $300NoNoMore than $300YesYesClientsUnlimitedNoNo Think of it like this: at your Christmas party, the food and drinks are like Santa’s bag of gifts – no dollar limit exists for employees enjoying them on business premises. But if you add a band or other entertainment, the costs can add up quickly, and if the total cost per employee exceeds $300, FBT kicks in. Keep it under $300 per person, and you’re in the clear. Christmas parties outside the office If you hold your Christmas party at an external venue, like a restaurant or hotel, it’s FBT-free as long as the cost per employee (including their family, if they come) is under $300. But remember, you can’t claim a tax deduction or GST credits in this case. FBT will apply if the cost exceeds $300 per person, but you can claim a tax deduction and GST credits. Good news: employers don’t have to pay FBT for taxi rides to or from the workplace because there’s a special exemption. FBT check for Christmas parties outside the office Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Employees onlyLess than $300NoNoMore than $300YesYesEmployees and their familyLess than $300NoNoMore than $300YesYesClientsUnlimitedNoNo Clients at the Christmas party If clients attend the Christmas party, there’s no FBT on the expenses related to them, no matter where the party is held. However, you can’t claim a tax deduction or GST credits for part of the costs that apply to clients. Christmas gifts Many employers enjoy giving gifts to their employees during the festive season. If the gift costs less than $300 per person, there’s no FBT, as it’s usually not considered a fringe benefit. FBT check for Christmas gifts Who attendsCost per personDoes FBT applyIncome tax deduction/Input Tax Credit available? Entertainment giftsLess than $300NoNoMore than $300YesYesNon-entertainment giftsLess than $300NoYesMore than $300YesYes However, FBT might apply if the gift is for entertainment. Entertainment gifts include things like tickets to concerts, movies, or holidays. Non-entertainment gifts—like gift hampers, vouchers, flowers, or a bottle of wine—are usually FBT-free if under $300. So spread the festive cheer, but keep an eye on the taxman to avoid surprises!

6-year rule

Aged care strategies Considering evolving policies and retirement needs, this issue navigates tax strategies, funding and transitions to aged care and discusses key considerations for this transition. Key Superannuation Strategies for Aged Care Superannuation is critical to funding aged care services in retirement. Proper planning around accessing superannuation can minimise tax impacts and optimise retirement income. Some of the key strategies are as follows: Transition to Retirement (TTR) Strategy If you’re between the preservation age and 65, you can access part of the super while working through a Transition to Retirement (TTR) income stream. This can provide an income boost or a way to gradually reduce working hours while receiving a steady income from super. Earnings on assets supporting a TTR pension are tax-free if you are 60 or over. Also, from age 60, withdrawals from the superannuation income stream are tax-free. Re-contribution Strategy: If the superannuation balance includes taxable and tax-free components, you can withdraw a lump sum and re-contribute it as a non-concessional (after-tax) contribution. This can reduce the taxable portion of the super, which can lead to lower taxes on super death benefits to non-dependents (such as adult children). Downsizer Contributions: If you’re 55 or older (since 1 January 2024), you can make a one-off, non-concessional contribution of up to $300,000 (per person) from the sale of the primary residence. This can help increase super savings and fund future aged care needs. Downsizer contributions are not subject to the usual super contribution caps and don’t require meeting a work test. Age Pension and Superannuation: Once you reach the pension age (increasing to 67), the superannuation balance will be counted in the assets and income tests for Age Pension eligibility. Effective super management may allow you to receive a partial Age Pension alongside superannuation income. Tax Considerations for Aged Care Various costs are involved in residential aged care, such as accommodation payments, means-tested care fees, and basic daily care fees. Proper planning is essential to manage these costs tax-efficiently. Accommodation Payments: Refundable Accommodation Deposits (RADs) are lump-sum payments to aged care facilities. They are not subject to tax. However, if you choose a combination of RAD and Daily Accommodation Payment (DAP), the DAP is paid from income and superannuation, which may have tax implications. Means-Tested Care Fees: Means-tested fees depend on assets and income, which includes superannuation. Careful planning can help reduce these fees by efficiently structuring income and asset withdrawals. Gifting: Assets to family members may reduce the assessable assets and income, helping to minimise aged care fees or increase pension eligibility. However, gifting rules apply, meaning you can only gift $10,000 per financial year or $30,000 over five years without affecting the Age Pension or aged care fees. Pension Income: If you’re receiving a pension from the super fund, income drawn from a tax-free pension account (for individuals aged 60 and over) will not be taxed. This can help manage tax obligations while covering aged care costs. Rental Income: If you rent out a family home to pay for aged care fees, rental income may be taxable. However, you may be able to offset some of this income through deductions for expenses such as interest on a mortgage, repairs, and maintenance. Using Super for Aged Care Costs: Drawing down superannuation in lump sums or as an income stream to cover aged care costs may be a tax-effective way to manage expenses, mainly if you are over 60 and withdrawals are tax-free. Retaining or Selling the Family Home When transitioning to residential aged care, one of the most significant decisions is whether to sell the family home or rent it out to fund the Refundable Accommodation Deposit (RAD) or other aged care fees. Selling may free up cash to pay a RAD, while renting may provide ongoing income but could have tax implications (assessable income) and impact Age Pension. Aged Care and Centrelink When calculating aged care fees or pension eligibility, superannuation and other assets will be assessed using Centrelink’s means tests. Deeming rates apply to financial assets, including superannuation income streams and bank accounts, to calculate income for Centrelink purposes. Lowering assessable income can help reduce aged care fees or increase government support. Home as an Exempt Asset: While you remain living in the home, it is exempt from Centrelink’s asset test. However, once you move into permanent residential aged care, the home is only partially exempt (up to a capped value), potentially increasing the assessable assets for aged care fees and Age Pension calculations. Transitioning to Aged Care – Key Considerations Transitioning to aged care in Australia is a significant life decision, and several key considerations need to be addressed to ensure a smooth and appropriate transition. These considerations include: Assessment and Eligibility Aged Care Assessment Team: An ACAT (Aged Care Assessment Team) or ACAS (Aged Care Assessment Service in Victoria) assessment is required to determine government-subsidised aged care services eligibility. The assessment evaluates the level of necessary care (home care, residential care, respite care). Types of Care: There are different care options, including: In-home care (for those who want to stay at home with support). Residential aged care (for full-time care in an aged care home). Respite care (short-term care to provide caregivers with a break). Retirement villages (offering independent living with access to services). Costs Upfront Fees and Ongoing Costs: Understanding the cost of aged care services is essential. This can include: Accommodation fees (refundable or non-refundable deposits for residential aged care). Means-tested care fees (based on financial situation). Basic daily fees (contribution toward care services). Additional services (for extra services, like premium amenities). Government Subsidies: The government heavily subsidises aged care services, but the level of subsidy is based on the individual’s financial assessment. Choosing the Right Aged Care Provider Location and Facility: Proximity to family and friends, the quality of the facility, and availability of activities and services should be considered. Visit different facilities to get a feel for the environment, staff, and overall care quality. Staffing and Services: Investigate staff-to-resident ratios, qualifications, and the quality of care services (e.g., medical care, recreational activities, and specialised services for conditions like dementia). Emotional and Psychological Impact Adjustment to Change: Moving to aged care can be an emotional process for the individual and their family. A support system is crucial to ensure the emotional well-being of the person transitioning, as they may feel a loss of independence or experience anxiety about the change. Family Involvement: Involving family members in decision-making can help ease the transition and provide emotional support. Legal and Administrative Issues Enduring Power of Attorney (EPOA): Legal arrangements for managing finances and healthcare decisions are essential. An EPOA allows someone trusted to manage financial and legal matters if the person cannot do so. Advanced Care Directives: These guide medical treatments and care preferences should the individual become unable to communicate their wishes. Health and Care Needs Medical Considerations: If the individual has specific health needs (e.g., dementia, physical disabilities, or chronic illnesses), it is essential to choose an aged care facility or home care provider that can meet these requirements with the appropriate medical care and support. Cultural and Personal Preferences Culturally Appropriate Care: Many aged care providers offer culturally sensitive services, including language support and community connections for non-English-speaking people. Personalization of Care: It’s important to consider how much the aged care provider can cater to personal preferences, such as dietary needs, religious practices, and lifestyle choices. Government Resources and Support My Aged Care: This government portal is crucial for information about aged care services, providers, and financial assistance. It helps individuals navigate the aged care system, guiding eligibility, services, and funding options. Considering these factors and seeking appropriate professional advice, the transition to aged care in Australia can be planned with care and sensitivity, ensuring the individual’s better quality of life. Superannuation Changes Reduction of the Downsizer Age to 55: Effective 1 January 2024, the eligibility age for downsizer contributions was reduced from 60 to 55. This allows more individuals to bolster their super balance by selling their family home. Legislative Cap on Superannuation Balance The government introduced a $3 million balance cap on superannuation, effective 1 July 2025. Individuals with super balances exceeding this cap will pay an additional tax of 15% on earnings on the excess. Conclusion Developing an effective aged care tax strategy involves carefully managing the superannuation, pension entitlements, and assets. Understanding the tax impacts of superannuation withdrawals, managing aged care costs, and planning around Centrelink and income tests can optimise the financial situation during retirement and aged care transitions. Consulting with a financial advisor can provide tailored advice to ensure compliance with regulations and maximise the benefits. Consulting an expert in aged care can help you make informed decisions about funding options, using assets (like the family home), and managing ongoing costs. They can also advise on government entitlements, such as the Age Pension.

INVESTMENT PROPERTY TAX Benefits, costs and key considerations If you’re considering investing in property, you must understand the tax consequences. In Australia, like many other parts of the world, owning an investment property offers potential tax benefits and costs. From claiming deductions on interest payments and holding costs to understanding the nuances of Capital Gains Tax (CGT), property investors need a comprehensive grasp on these matters to make the most out of their investments. Investing in property can be a wise financial move, but it’s essential to understand the benefits and costs involved, especially regarding taxes. Here, you’ll get an overview of how owning an investment property can impact your taxes, helping you make informed decisions. Property investment tax benefits Interest payments and holding costs Owning a rental property comes with its share of expenses. The list goes on, from interest payments, updates, upkeep, and local council fees to fees for property management. But here’s some positive news: many of these costs can be claimed as tax deductions if your property is up for rent or already rented out. For many property owners, the interest accumulating on a mortgage used to purchase a rental property can be claimed as a tax deduction. Other often-claimed deductions include fees for property management, land taxes, and upkeep-related costs. This upkeep can range from general cleaning and landscaping to insurance coverage and repairs. Learn to grow your business and better understand your finances. Schedule a complimentary consultation with us today. Claiming depreciation on rental assets When you purchase items for your rental property, such as new appliances, they lose value over time due to wear and tear. This decline in value is known as depreciation. You can claim this loss in value as a tax deduction, often referred to as tax depreciation or capital allowance, spread across the useful lifespan of that item. Claiming for construction and renovations You can claim these expenses as deductions if you’ve undertaken construction or renovation projects at your rental property. Typically, these capital works deductions are spread out throughout 25 to 40 years. The exact time frame will depend on the construction’s start date, purchase date, and intended use. Offsetting losses with negative gearing When your rental property’s expenses exceed earnings, resulting in a net loss, this is termed “negative gearing.” The upside to negative gearing is that you might be able to leverage this loss to counterbalance income from other sources, ultimately lowering your taxable income for the year. A table summarises the tax benefits of property investment in four categories: holding costs, depreciation on assets, construction/renovation deductions, and negative gearing advantages. Tax implications of property investment Owning an investment property brings with it various tax considerations. Capital Gains Tax (CGT) If you decide to sell your investment property, any profit you realise could be subject to Capital Gains Tax. We’ll discuss CGT in more detail in this article. Tax on rental income The revenue generated from your rental property is subject to taxation. This rental income is added to any other income you may have, such as wages or investment earnings, and the total is taxed according to your income tax bracket. Asset depreciation Assets such as appliances and furniture can be claimed as depreciation for tax deductions on your tax return; however, it’s essential to maintain detailed records and a depreciation schedule. Deductibility of property expenses Certain expenses related to your property are tax-deductible, while others are not. Expenses associated with the depreciation of assets or improvements to the property’s structure can be claimed as deductions at the rate allowed by the ATO. On the other hand, expenses incurred during the purchase or sale of the property are generally not eligible for tax deduction. GST considerations If you lease a commercial property to another business for rental income, you may have to pay Goods and Services Tax (GST). Tax regulations can be complex, so if you’re ever uncertain, it’s wise to consult with us or refer to the Australian Taxation Office for guidance. Tax considerations for property investment: Capital Gains Tax (CGT) Tax on rental income Asset depreciation Deductibility of property expenses GST considerations Four types of tax on investment property Income tax The income from your rental property is subject to tax, just like your regular income. When lodging your income tax return, you must include the rental income alongside any other earnings, such as your salary or profits from other investments. Suppose your property’s expenses exceed its rental income, creating a loss (known as “negative gearing”). In that case, you can deduct this loss from your overall income, potentially reducing your tax liability. Some investors favour this strategy over “positive gearing,” where the property generates a profit because it can decrease the taxes they owe. Fortunately, the Australian Tax Office (ATO) allows property investors to deduct various property-related expenses from their rental income, which can help maintain the profitability of their investment. Immediate deductions Immediate deductions refer to expenses you can claim as tax deductions in the same financial year. These include costs for advertising for tenants, council and water rates, land tax, interest on your mortgage, and expenditures for repairs and maintenance, etc. Long-term deductions Some costs can be spread out over multiple years. A good example is “depreciation,” which lets you subtract a portion of the property’s value each year to account for wear and tear and the aging of the building and its fixtures. Remember, not every expense is deductible. You can’t subtract costs like the initial tax paid when buying the property (stamp duty), your mortgage payments, or any expenses your tenant covers. Capital Gains Tax (CGT) Are you thinking of selling your rental property? Be prepared for the potential of Capital Gains Tax. If you make money when selling your rental property, that profit is seen as a “capital gain.” This profit needs to be reported on your yearly tax return. The extra tax you owe because of this added profit is called Capital Gains Tax or CGT. The ATO has rules that might let property investors avoid paying some or all of the CGT. Here are some of the exceptions and special rules: Main Residence (MR) Exemption This rule applies if the property is your primary home. Capital Gains Tax Property 6-Year Rule This rule allows you to treat a property as your primary residence and apply the principal residence exemption from Capital Gains Tax. Note that a family can only have one principal place of residence at any given time. The Six-Month Rule A rule that offers some flexibility when moving between properties. 50% CGT Discount The 50% Capital Gains Tax (CGT) Discount allows you to halve the capital gain on your property when calculating tax, provided the property was held for more than 12 months. This discount is designed to encourage long-term property investment. Stamp Duty Tax When you buy an investment property, you must pay a stamp duty tax. Think of it as sales tax for purchasing property. This tax is due when the property’s ownership changes hands from the seller to the buyer. That’s why some also call it transfer duty. The Australian Taxation Office (ATO) doesn’t let you claim this as a tax deduction on your income tax return, but it can be added to the asset’s cost base for CGT purposes. So, property investors should check how much they’ll have to pay before buying a property, as it can affect their rental income and expenses. Stamp duty varies depending on: The state you’re in The property’s price If you’re a first-time buyer Generally, every property transfer, even among families or different ownership structures, requires stamp duty. Only a few exceptions exist. While stamp duty is an immediate concern for property investors, you should also be aware of other tax obligations. These can include capital gains tax, land tax, and claiming various tax deductions. Land Tax Land tax is different from stamp duty. While you pay stamp duty just once when you buy a property, land tax is an ongoing charge based on the land’s value unless the property is your primary home (often referred to as Principal Place of Residence or PPOR). Every state and territory has a land tax rate based on the land’s “unimproved value.” This means that the value of buildings, walkways, landscaping, or fences on the land is not included when calculating land tax. Land tax rates and thresholds for each state or territory are available on the Revenue Office websites for each state. It’s worth noting the Northern Territory is unique because property investors there don’t have to pay land tax. If you’re a property investor, you must know these ongoing tax obligations, which can affect your rental income and expenses.

FAMILY LAW FINANCIAL SETTLEMENTS

Individuals and Business Checklists to the website

P r a c t i c e U p d a t e July 2024

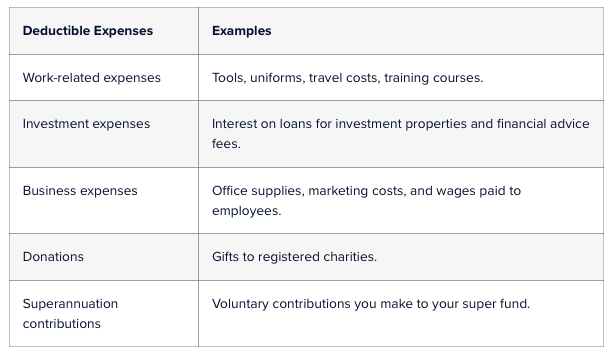

Ways to get ready for tax time The end of the financial year on 30 June 2024 is fast approaching, so here’s a quick checklist to help you prepare in advance and maximise your tax time benefits. Understand your sources of income Income can come from all sorts of areas. Interest earned from bank accounts Dividends received from shares Employee share options Capital gains received from the sale of an asset Rental income from an investment property Redundancy payments Any taxable Centrelink payments Deductions Undoubtedly, it is the most contentious area of tax returns. This could include expenses incurred and not reimbursed, which may reduce tax liability. Some common deductions are: Work-related expenses Home office expenses Self-education and professional development Registrations, subscriptions, memberships Vehicle and travel expenses Protective clothing, laundry and dry-cleaning expenses Tools and equipment, including depreciable assets (such as laptops) Accountant or tax agent fees Personal super contributions Investment income expenses Income protection insurance premiums Offset capital gains against capital losses Disposal of shares or any other form of investment may cause capital gain. You may consider disposing of any assets you know are trading at a loss. The resulting capital losses can be offset against the capital gain. Don’t forget the upcoming tax changes may mean that from 1 July, you’re paying less tax, which might affect when you decide to divest any investments and incur a capital gain – this year or next. Also, be careful if you sell shares at a loss and buy them back in the new tax year. The ATO takes a hard line against so-called “wash sales”. This refers to the sale of an asset before the year-end and the purchase of a substantially identical asset immediately after the year-end. The ATO regard the purchase and the sale as effectively the same asset and has issued a Tax Ruling, which states that they can apply the anti-avoidance provisions to cancel any tax benefits and apply penalties. Document your donations It’s great to give to your charity of choice, but don’t forget your potential tax deductions. So, hang on to your receipts and record your donations. Ensure that the charity is a deductible gift recipient. Understand the Medicare levy If you earn over a certain amount, you must pay the 2% Medicare levy to help fund the private health system. But there’s a potential rebate available if you are a high income earner and take out private health insurance. So, you might want to work out your best approach, particularly if you have earned more than last year. Get your retirement income right If you’re retired, the good news is you can earn a higher income level before you start paying taxes. But it can depend on your age and the type of income you receive, so it’s a good idea to get across all the rules with your accountant. Get your investment property affairs in order If you’re renting a property out, you’ll probably be aware that there are plenty of tax deductions you can claim for things like depreciation, the cost of repair and maintenance, interest costs on your loan and fees that you pay for a real estate agent to manage your property. As usual, the rules can (and do) change, so check all the latest expenses you can claim here. Home Office If you are employed but work from home, occasionally or all the time, you are entitled to deductions for costs arising from working at home. The expenses that you can claim include: Heating, cooling and lighting Cleaning costs Decline in value (depreciation) of home office furniture and fittings, office equipment and computers (for items over $300) Computer consumables, stationery, telephone and internet costs Items of capital equipment (such as furniture, computers and associated hardware and software) which cost less than $300 can be written off in full immediately With many retailers running End of Financial Year specials, any purchases you make now can be deducted from this year’s tax return, so from a cash flow point of view, you can minimise the time between purchase and tax deduction! Alternatively, you can claim the ATO’s concessional 67 cents per hour fixed rate to include several working-from-home deductions in one simple, easy-to-use amount. The rate includes the additional running expenses you incur for: home and mobile internet or data expenses mobile and home phone usage expenses electricity and gas (energy expenses) for heating, cooling and lighting stationery and computer consumables, such as printer ink and paper. To use the fixed rate, you must have kept a record of all your working from-home hours for the entire year (e.g., a diary, timesheets or rosters), and you must have one item of substantiation for each item claimed (e.g., a heating bill). The fixed-rate does not include deductions for work-related use of technology and office furniture such as chairs, desks, computers, bookshelves or repairs to these items. Cleaning costs are also excluded. These costs can be claimed separately, so remember to keep those receipts. Car expenses If you use the log-book method, now is the time to check that your logbook is current and that you have all the receipts, invoices and journey records you need to calculate and substantiate your claim. Using the cents per kilometre method, you will still need a record of all work-related journeys during the year. Mobile Phone If you used your mobile phone for work purposes, you could claim a deduction for the business-related use. Ensure you have compiled your phone bills and have kept a log of your business/personal use over four weeks. That percentage can then be applied to the whole year. It’s important to remember that you can’t claim a separate deduction for mobile phones if you have claimed the 67 cent/hour fixed rate for working from home. Prepay expenses You can claim a tax deduction this year for expenses which wholly or partly relate to next year. So, if you have some spare cash, consider paying things like union fees, professional subscriptions and annual insurance premiums in advance to accelerate the deduction. If you have a geared asset like a rental property and have capital to inject, some lenders may allow you to prepay 12 months of interest on your investment loan. This will effectively bring forward your tax deduction into the current year and could help offset any capital gains or additional income you’ve earned. Make a tax-deductible super contribution If you have some spare cash, consider contributing to your super fund. Suppose your contributions (including those made on your behalf by your employer) do not exceed $27,500. Your cap may be higher if unused concessional contribution cap amounts are unused. This can be a great way to boost your retirement savings and claim a tax deduction for the personal contribution. Co-contributions: Low or middle-income earners who make personal super contributions may receive a government co-contribution, up to a maximum of $500. Employee salary sacrifice: an agreement with your employer to give up part of your salary (thereby reducing your taxable income) and invest it into super to boost your retirement savings. Spouse contributions: A tax rebate (up to $540) may be available for after-tax contributions to super on behalf of a low-income spouse. Timing: Contributions must be in your super account before 30 June, or they will count against the next financial year’s limits. If you’re between 67-74, you won’t need to satisfy the ‘work test’ before making non-concessional contributions. However, you’ll still need to satisfy the work test requirement if you want to claim a tax deduction on your personal contribution. The payment must be made by June 30th, and you must advise your super by providing a valid ‘notice of intent to claim a deduction for personal superannuation contributions’ to your super fund and have received written acknowledgement. Small business Initiative during EOFY Checklist of to-do before year-end Review year-to-date figures to determine likely tax liability Consider strategies for management of the likely tax position Determine dividends to be declared for companies Prepare distribution minutes for trusts Consider owners’ remuneration and optimise tax outcome Small Business Entities – cash vs. accruals/prepayments/depreciation Make superannuation payments as they are only deductible when paid Debtor analysis – consider bad debts/timing of invoicing Creditor analysis – bring forward expenses to get a tax deduction Stocktake – undertake a stock take and consider obsolete stock Plant and equipment – consider any new equipment needed and ensure it is available and ready for use before June 30 Fringe Benefits Tax – if FBT return is not lodged, consider a private portion of expenses and GST adjustments Capital Gains Tax – consider the sale of any investments and prepare likely tax calculations Asset write off If so, look to utilise the “instant asset write-off” measure. Provided your business has a turnover of less than $10 million, this allows you to claim an immediate tax deduction for all capital purchases costing less than $20,000 rather than depreciating the cost over several years, as used to happen. This is great for tech items such as computers, tablets and phones, as well as tools and equipment for tradies, office furniture and even motor vehicles (though any cars will probably need to be second-hand, given the $20,000 limit!). Remember, besides purchasing, the asset you acquire must be used or available in your business. So, realistically, you need to get the item delivered and installed by 11:59 PM on 30 June 2024 to secure the tax deduction. If you order something now for delivery and installation in July, you won’t be able to claim the deduction this tax year. Note that the instant asset write measure will also be available in 2025. Maximise your tax-deductible debt Loans for private purposes are not tax deductible. Review whether refinance options may be available to split your deductible vs non-deductible debt. Determine whether loan repayments can be restructured, as the new rules limit the deductions available against vacant land. Write off bad debts If debtors are not recoverable after all action has been taken, write off the bad debt before June 30 to account for the expense. Ensure GST is adjusted. Write off slow-moving or obsolete stock Review your stock holding. If the market value is lower than the cost of the stock, you can obtain a deduction for the difference. Utilise unrealised capital losses Ensure you take advantage of capital losses within your group. Consider preparing distribution minutes that use group losses. Check depreciation rates on plants and equipment Review depreciation schedules for any scrapped plant and equipment that can be written off. Review the effective lives of equipment and consider whether you can increase the depreciation rate. Check your access to refundable franking credits Look for opportunities before June 30 to access any refundable franking credits. Consider whether any loss entities could result in a flow of highly franked income, resulting in a refund. Claim eligible research and development activities When engaged in research and development activities, clearly document the activities and costs relating to those activities to take advantage of R&D Tax Offsets. Plan for your tax position before June 30 Understand your options to reduce or defer tax payments. Plan your cash flow for tax instalments and the tax due on tax return lodgements. Identify opportunities to vary tax instalments and improve cash flow. Implement the tax planning measures listed above, as well as other savings. Other considerations Planning for one-off transactions – e.g. Business sales or purchases. Self-managed Super Fund (SMSF) – do you have an SMSF? Consider the impact on the business. Purchase of property or business premises. Consider the relevance of existing accounting systems and consider new technology.

Practice Update - June 2024

BUDGET 2024-25 OVERVIEW

Business valuation

How do Bucket Companies work? What is a Bucket Company? Ensuring a business remains profitable is one of the most important responsibilities of a business owner. So, if the business starts to generate a healthy profit, there needs to be a plan. While maximising deductions has its place in any tax planning strategy, a tax minimisation strategy that solely relies on deductions can result in sacrificing profit to lower tax when other options are available. With you and your family relying on the profits generated by your business to fund your lifestyle, it’s essential to understand the most tax-effective manner for distributing income and the best business structures that allow you to do so. Consider how a bucket company might fit into your overall tax planning strategy. Uses of Bucket Companies A bucket company (otherwise known as a corporate beneficiary) is a company set up as a trust beneficiary. This arrangement allows any income the trust distributes to the bucket company to be payable at the company tax rate, currently 25% (only if it is a base-rate entity), as opposed to the individual marginal tax rate (the top tax rate for individuals for 2023-2024 is proposed to be 47%, including the Medicare levy). They’re called bucket companies because they sit below a trust like a bucket and are used to distribute income to it. It is important to remember that there are rules around family trusts and structures within a family group. Otherwise, family trust distributions tax may apply. How do Bucket Companies work? There are generally three elements present for a bucket company: There is usually a trust with surplus income to distribute. The corporate beneficiary must fall within the definition of ‘beneficiary’ under the trust deed. Consider whether the bucket company is part of a family group. Who should hold the company’s shares? One of the main reasons bucket companies are used is to access the tax benefits they provide, and you should keep this in mind when deciding who holds the company’s shares. If an individual holds the shares, there is less flexibility in how the dividends can be distributed; they will need to be distributed according to the shareholder percentage. However, if another kind of trust holds the shares, the excess profits may be distributed, allowing for less total tax paid. Tax rates of bucket companies The bucket company pays the corporate tax rate, which could be 25% or 30%, depending on the type of company. If the company is a base rate entity, a company tax rate of 25% will apply; however, if it is not, the company tax rate will likely be 30%. Taxing trust income The general principle is that a trust’s net income is taxed by its beneficiaries; individuals and company beneficiaries pay tax on their portion of the trust’s income at the rates that apply to them. The highest marginal tax rate for individuals (not including the Medicare levy) at the time of writing this article is 45% for people with taxable income of $180,000 or more. There is a flat tax rate of 30% for non-base rate entity companies. Due to the discrepancy between the highest marginal tax rate for individuals and the company tax rate, there is at least a 15% savings potential. To illustrate, on an income distribution of $100,000, a corporate beneficiary would pay at least $15,000 less tax. Commit to distributions You must ensure that when you distribute to the bucket company for the financial year, you also distribute the same amount to the company’s bank account before lodging the tax return. In particular, trusts must distribute to corporate beneficiaries; otherwise, the Unpaid Present Entitlement (UPE) rules may be triggered. What can be done with the money in the Bucket Company? So far, in this article, we have looked at how bucket companies can help individuals save tax by paying out dividends at company tax rates. However, this is not the only bucket company strategy available. A bucket company can also hold long-term investments, such as shares, properties, or investments. In this regard, the bucket company becomes an investment company that can generate another source of income for the owner. Companies cannot access the 50% Capital Gains Tax discount, but other compelling reasons exist to use a company structure. Getting money out of the Bucket Company As has been established, the trust distributes the income to the bucket company, which begs the question: How do you get money from a bucket company? There are three ways to extract money from a bucket company: Pay dividends to the shareholders. Because the dividend has been taxed at the company rate, the shareholder will receive a franking credit to the extent that the tax has already been paid. An individual will include the dividend income as taxable income. Any excess franking credits are refundable, or top-up tax may be required depending on the shareholder’s marginal tax rate. A loan from the bucket company. As with any other loan, you must pay back the principal and interest to the bucket company. The loan is a special type called a Division 7a Loan, with requirements you will need to be mindful of. A separate discretionary trust structure can receive the dividends. Whereas the first method requires profits to be distributed according to shareholding and the second method incurs interest, this last method distributes profits according to the Trust deed. For example, using a discretionary trust as a shareholder of the bucket company allows you to make the largest distribution to an individual with the lowest marginal tax rate. Note that there may be other rules to satisfy or consider, such as Section 100A. Will a family trust structure allow a Bucket Company? To function as intended, a bucket company must be an eligible beneficiary of a family trust. As a result, you must read the trust deed to ensure the bucket company falls within the general class of beneficiaries. Additionally, a Family Trust Election may be needed depending on the structure. Consider the family group, which may define or impact who the beneficiaries are. Appropriate bucket Company strategy While bucket companies are generally useful for investors and business owners, and there is no doubt that they can be one of the most tax-effective strategies, they may not be ideal for your unique situation. A bucket company strategy may be of benefit if you are any of the following: A business owner who wants to build a nest egg for their family. A business owner who experiences significant fluctuations in income from one financial year to the next. For business owners coming up to retirement or looking to sell their business and who won’t be earning as much business income moving forward as a result Using a bucket company will not work if caught under the Personal Services Income (PSI) rules. These rules prevent individuals from reducing or deferring their income tax by diverting income they receive from their personal services through companies, partnerships, or trusts. We encourage you to seek professional advice when deciding whether a bucket company suits you.

Practice Update March 2024

IMPACTS OF THE REVISED STAGE 3 PERSONAL TAX CUTS

CGT discount If you are selling a CGT asset, delaying the sale may be worthwhile to qualify for the CGT discount. CGT assets include land, buildings, shares, rights and options, leases, units in a unit trust, goodwill, contractual rights, licences, foreign currency, cryptocurrency, convertible notes, etc. Under the discount rules, when you sell or otherwise dispose of an asset (for instance, give the asset away), you can reduce your capital gain by 50% if both of the following apply: You owned the asset for at least 12 months, and You are an Australian resident for tax purposes. Regarding the first requirement, you must own the asset for at least 12 months before the ‘CGT event’ (usually a sale) happens. The CGT event is the point at which you make a capital gain or loss. You exclude the day of acquisition and the day of the CGT event when working out if you owned the CGT asset for at least 12 months before the ‘CGT event’ happens. To be clear: If you sell the asset and there is no contract of sale , the CGT event happens at the time of sale. If there is a contract to sell the asset , the CGT event happens on the date of the contract, not when you settle. Property sales usually work this way. If the asset is lost or destroyed , the CGT event happens when: you first receive an insurance payment or other compensation. if there is no insurance payment or compensation when the loss occurred or was discovered. You could count an asset’s previous ownership towards your 12-month ownership period if you acquired it: through a deceased estate if the asset was acquired by the deceased on or after 20 September 1985 through a relationship breakdown – you will satisfy the 12-month requirement if the combined period your spouse and you owned the asset was more than 12 months. as a rollover replacement for an asset that was lost, destroyed or compulsorily acquired if the period of ownership of the original asset and the replacement asset was at least 12 months. From 8 May 2012, the full CGT discount is not available for capital gains made by foreign or temporary residents. Returning to the theme of the article, if you held an asset for 11 months and were upon sale on track to make a capital gain of $30,000, then by delaying the sale by one month, you could reduce that gain to $15,000 by taking advantage of the 50% discount. Note that as well as non-residents, the 50% discount is not available to companies. SMSFs and trusts are both eligible (though the discount is 33% for SMSFs). Super tax offset If your spouse is a low-income earner, adding to their superannuation could benefit you financially. If you’d like to help them by putting money into their super, you might be eligible for a tax offset while potentially creating additional opportunities for both of you. Eligibility To be entitled to the spouse contributions tax offset: You must make a non-concessional (after-tax) contribution to your spouse’s super. This is a voluntary contribution made using after-tax dollars, which you don’t claim a tax deduction for. You must be married or in a de facto relationship. You must both be Australian residents. The receiving spouse’s income must be $37,000 or less for you to qualify for the full tax offset and less than $40,000 for you to receive a partial tax offset. Benefits If eligible, you can generally contribute to your spouse’s super fund and claim an 18% tax offset on up to $3,000 through your tax return. To be eligible for the maximum tax offset, which works out to be $540, you need to contribute a minimum of $3,000, and your partner’s annual income needs to be $37,000 or less. If their income exceeds $37,000, you’re still eligible for a partial offset. However, once their income reaches $40,000, you’ll no longer be eligible for any offset but can still make contributions on their behalf. Contribution limits You can’t contribute more than your partner’s non-concessional contributions cap, which is $110,000 per year for everyone, noting any non-concessional contributions your partner may have already made. However, if your partner is under 75 and eligible, they (or you) may be able to make up to three years of non-concessional contributions in a single income year under bring-forward rules, which would allow a maximum contribution of up to $330,000. Another thing to be aware of is that non-concessional contributions can’t be made once someone’s super balance reaches $1.9 million or above as of 30 June 2023. So, you won’t be able to make a spouse contribution if your partner’s balance reaches that amount. There are also restrictions on the ability to trigger bring-forward rules for certain people with large super balances (more than $1.68 million as of 30 June 2023). Joint tenants and tenants in common When buying a property with another person, you are given the option of how to be registered on the title of the property with them: joint tenants vs tenants in common. But what is the difference between the two, and is one better than the other? In this article, we explain everything you need to know. What is Joint Tenants? Joint tenants (also known as joint proprietors) means you own 100% of the property jointly with the people registered as joint tenants with you. Practically this means: When joint tenants die, the surviving owner(s) automatically become entitled to be registered as the sole owner(s) of the whole of the interest in the property. This means that any property owned in joint tenancy do not form part of a deceased’s estate, rather their interest automatically goes to the surviving owner(s). This is called “the right of survivorship”. You even split the property’s profits, losses, and risks. You cannot have an uneven share of the property. All joint tenants own the property 100% jointly. For tax purposes, the shares are even. What is Tenants in Common? Tenants in common means you have a defined ownership share of a property title. This can be 50-50, 60-40, 99-1 or any other combination. Practically this means: On the death of either of the owners, the deceased’s interest in the property passes to his or her beneficiary (not necessarily the surviving owner on the title). The beneficiary is dictated by the deceased’s Will or if they do not have a Will by State law. The defined ownership share splits the property’s profits, losses, and risks. Can you do both Tenants in Common and Joint Tenants at the Same Time? Yes, you can if you have three or more owners on the title. For example, persons A and B hold a 50% share of the property as tenants in common jointly, while person C holds their 50% share as a tenant in common individually. Practically this means: On the death of either person A or B, who holds their 50% share jointly, the survivor of A or B will get the full interest of the deceased share. Person C will not have any claim to this share as they did not hold that 50% share jointly. If Person C passes away, Persons A and B will have no automatic interest in Person C’s share of the property. Rather, person C’s share in the property will go to their beneficiary in accordance with their Will or State law if no Will exists. Touch base with us if you would like more advice about the ownership structure you should adopt when acquiring property. Superannuation downsizer Are you looking to boost your superannuation balance as you near retirement? Put simply, the intention of the downsizer contribution rules is to allow older Aussies to sell their current home and use the proceeds to contribute to their super account. Starting 1 January 2023, new rules have lowered the minimum eligibility age to allow people aged 55 and over to access downsizer contributions. Originally, the minimum age was 65, but this has progressively been lowered to age 55. The lower age limit (55 years) is based on your age when you make the contribution, and there is no upper age limit . Normally, once you reach age 75, the super rules prevent you from making voluntary contributions, so a downsizer contribution presents a rare opportunity to top up your super. There is no work test requirement to make a downsizer contribution. In fact, there is no requirement for you to have ever been in paid employment. However, you can’t claim a tax deduction for a downsizer contribution. Contribution limits Under the downsizer rules, you are allowed to contribute up to $300,000 ($600,000 for a couple) from the sale proceeds of your eligible family home. The contribution limit is the lesser of $300,000 and the gross actual sale proceeds. This means if you gift your home to a family member and the sale proceeds are $0, you cannot make a contribution. Any debt or remaining mortgage on the property does not impact the amount you are permitted to contribute to your super account. Eligible homes While the downsizer rules are generous, ensuring your home is eligible before you sell is essential. The key criteria are: You must have owned your property for a continuous period of at least 10 years. This is usually measured from the date of your original settlement when you purchased the property to the settlement date when you sell it. The property being sold must be your family home (main residence) at the time of the sale, or it must be partially exempt from capital gains tax (CGT) under the main residence exemption. The home you sell must be in Australia. Some types of property are not eligible under the downsizer rules. These include an investment property you have not lived in, caravans, houseboats and other mobile homes. Vacant blocks of land are also ineligible. If you sell your home and want to make a downsizer contribution, you are not required to buy a new home with any sale proceeds. That is, there’s no requirement to buy a cheaper or smaller home after making your downsizer contribution, so you can even decide to purchase a more expensive replacement home. Caution The costs involved in selling a family home can be substantial. If you purchase another home, sales commissions, moving costs, stamp duty, and land taxes mount up, so think carefully before deciding to downsize. Remember, selling a large home and downsizing to a smaller property does not always release much excess capital (particularly in a capital city), so do careful calculations on how much you will have left to contribute to super before selling.